Dorman products (DORM): quality compounder hiding in the aftermarket

138,000 SKUs, 25 years without a revenue decline, and a 30% discount to fair value.

As I’ve mentioned in notes - I have a new position. A boring quality value compounder which I bought at a discount. It’s Dorman Products (DORM). Here I share all the analysis that went into consideration. I promised to write on all new positions. This post comes a bit late. But it’s been a week, thesis holds and the recent rally did not wipe all of the MoS.

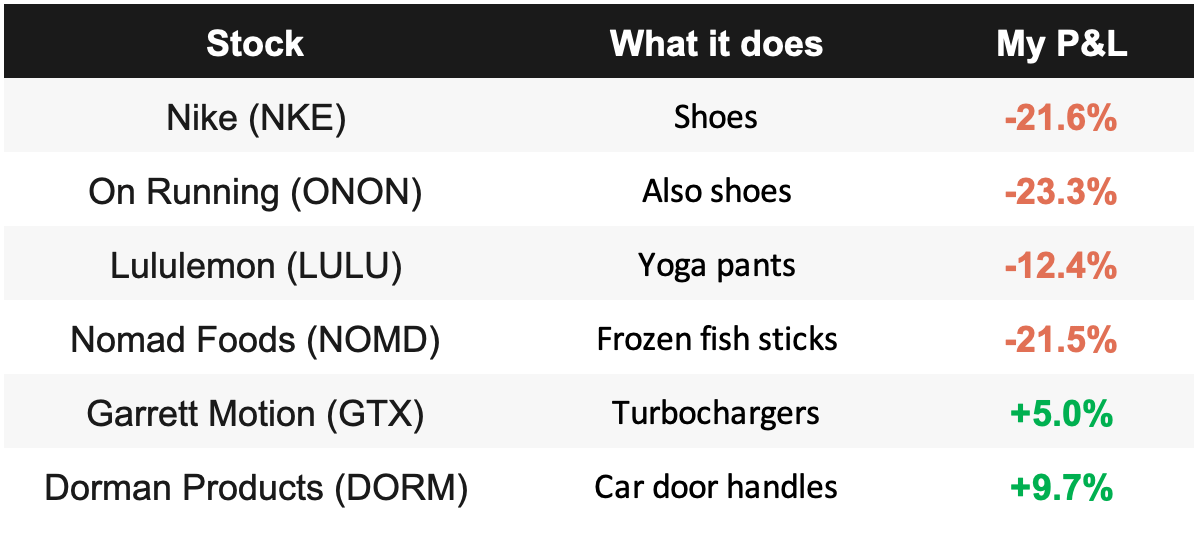

Speaking of the recent rally - here is the current state of my portfolio. It still feels like garbage. But I stand behind most of my positions. There is still capital to deploy and that’s what I am working on right now.

The one stock that’s quietly making money sells brake hardware, exhaust manifolds, and window regulators. Not AI. Not cloud. Not athleisure. Replacement auto parts.

There’s a lesson in this and it took me a while to see it.

What Dorman actually does

When the window motor on your 2014 Honda Civic dies, you have two choices. Go to the dealer and pay $400 for an OEM part. Or your mechanic orders a Dorman part for $120 that fits the same, installs the same, and often lasts longer because Dorman actually fixed the design flaw that made the original fail.

That’s the business. Dorman reverse-engineers parts that break on cars, improves them, and sells them to mechanics and DIY enthusiasts through distributors like AutoZone and O’Reilly. They have 138,000 different parts in their catalog. Last year they introduced 5,335 new ones.

The key detail: about a third of what Dorman sells has no aftermarket alternative. They’re the only option between the dealer and nothing. That’s not a brand story - it’s an engineering moat. You can’t copy a reverse-engineered transmission control module by putting a different label on a Chinese generic. You need electrical engineers who can decode proprietary software, test it, and certify it works. Dorman has been doing this for 15 years. Their competitors haven’t started.

Why aftermarket is a compounder’s game

Here’s a number I keep coming back to: the average car on American roads is 12.8 years old. That’s a record.

Cars don’t get younger. Every year a car stays on the road, it needs more parts. Window regulators fail. Brake calipers seize. Exhaust manifolds crack. Electronic modules glitch. This isn’t cyclical demand that depends on consumer confidence or interest rates. It’s entropy. Physics doesn’t care about the Fed.

The aftermarket grows when car sales are strong (more cars on the road eventually). It also grows when car sales are weak (people keep older cars longer). The only scenario where it shrinks is if everyone stops driving, which hasn’t happened in a hundred years.

And the mix is shifting in Dorman’s favor. Modern cars have more electronics, more sensors, more modules that can fail. A 2024 vehicle has roughly 3x the electronic content of a 2010 model. When a $15 mechanical part becomes a $200 electronic module, the aftermarket grows without a single additional car on the road.

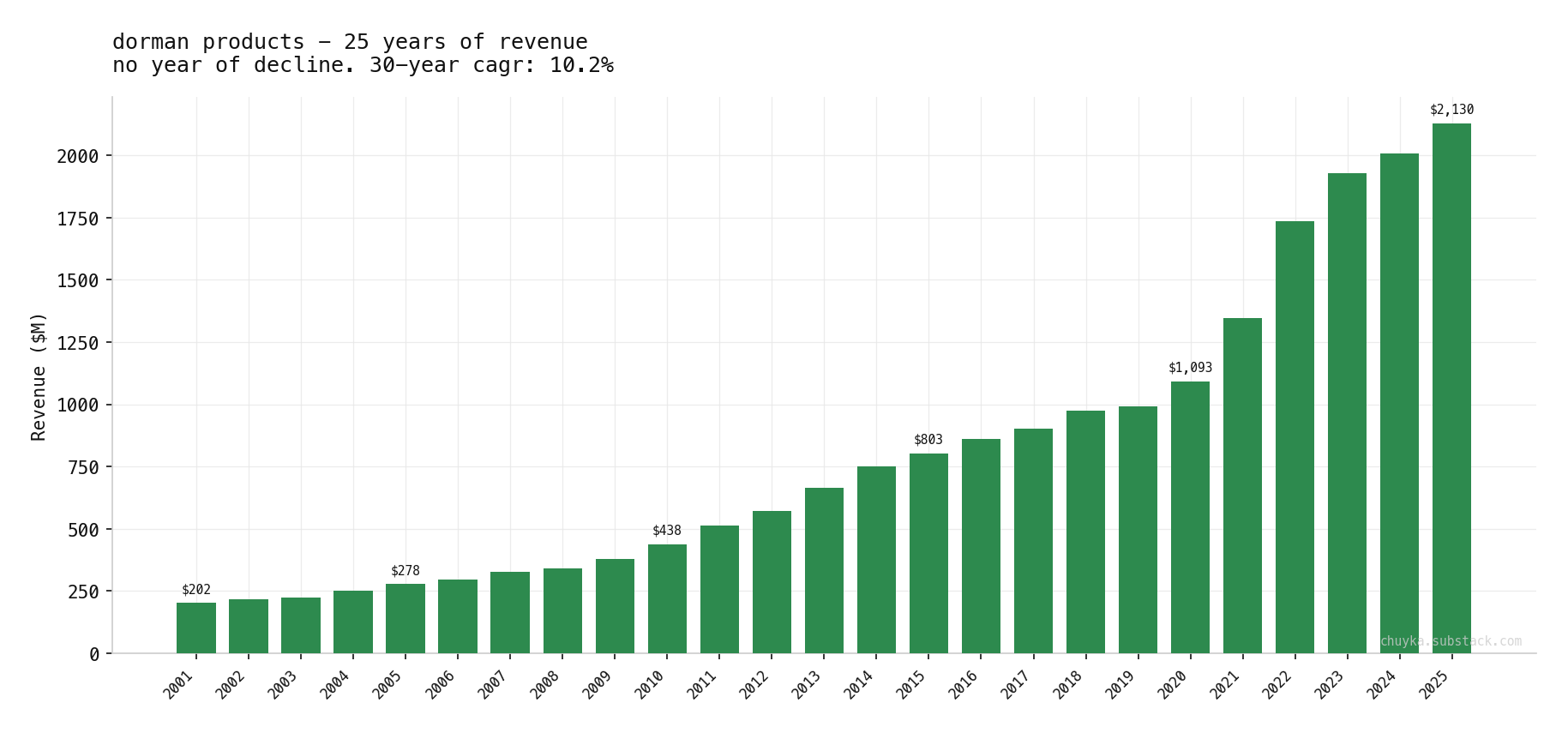

Dorman’s revenue hasn’t declined in 25 years. Not during the financial crisis. Not during COVID. Not during the tariff wars. The 30-year revenue CAGR is 10.2%. I haven’t found another business with that consistency. Take that with a grain of salt, it’s been just under a year, that I’m back to active stock-picking.

Is Dorman Products actually a quality business?

Good story is not enough. “Cars get older, parts break” is a nice narrative, but narratives don’t compound. Capital does. I need to know whether Dorman earns a real return on the money it puts back into the business - or whether it’s just growing revenue while destroying value.

I’ve been working through a framework for this. It comes from John Huber at Saber Capital (check out his substack, it’s a goldmine, now archived) - a fund manager who thinks about quality in terms of what the next dollar of invested capital earns, not what the historical average looks like. The concept is called Return on Incremental Invested Capital, or ROIIC.

The ROIIC idea is simple. Take the change in net income over 10 years. Divide by the change in capital invested over the same period. If the business earned $100M more than a decade ago and deployed $500M of new capital to get there, the incremental return is 20%. Every dollar invested created 20 cents of new annual earnings.

Headline ROIC - the number most screeners show - tells you about the average return across all capital ever deployed. A business that earned 25% in 2005 and earns 10% today might show 18% headline ROIC. Looks fine. But the marginal return is collapsing. ROIIC catches that. The investor who buys today is buying the marginal future, not the historical average.

ROIIC is a great indicator of quality. We must bear in mind that it has a trailing nature and past performance does not guarantee future results. But it is still a great way to analyse a company in numbers terms.

I’m writing a full post on this framework - the math, the methodology, how I apply it across my portfolio. For now, here’s what it shows on Dorman.

What the DORM ROIIC numbers say

Three things stand out.

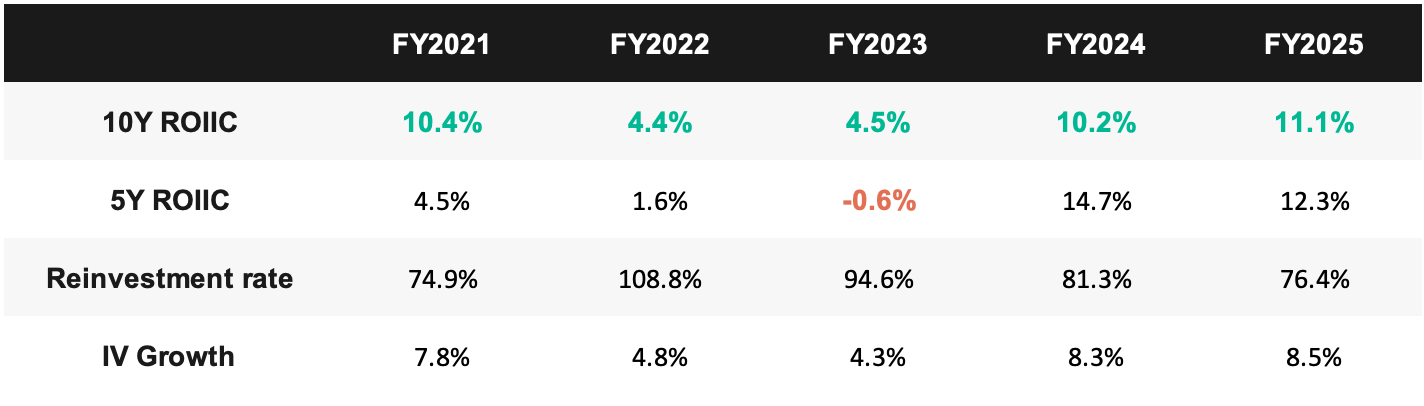

First, the V-shape. ROIIC compressed from 10.4% to 4.4% in 2022-2023, then recovered to 11.1%. That was in my view the SuperATV acquisition digesting. Dorman bought a powersports parts company, funded it partly with debt, and spent two years integrating. Capital went up, earnings hadn’t followed yet. By 2025, the deal is earning and ROIIC is back above pre-acquisition levels.

Second, the 5-year is higher than the 10-year. 12.3% vs 11.1%. This is the recovery signal - recent capital is earning better than the long-run average. The SuperATV acquisition drag is washing out of the shorter window. When the 5Y is below the 10Y, the business is deteriorating. When it’s above, the business is improving. Dorman is improving.

Third, the reinvestment rate is 76%. Dorman puts three quarters of its earnings back into the business. Not buybacks. Not dividends. Back into new SKUs, new distribution, new engineering capability. And it earns 11% on every reinvested dollar. That’s management vote of confidence for their business engine.

Pop the the hood

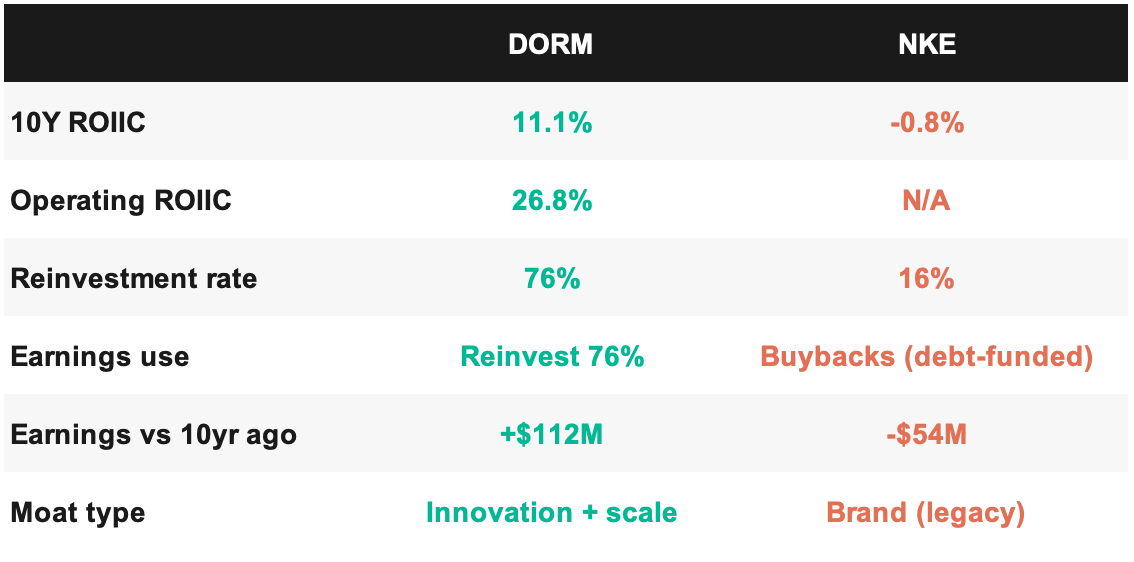

There’s a second lens on this that I find even more interesting. When I strip out the financing costs - the interest on the debt Dorman took on for acquisitions - and look at the pure operating return on tangible capital, the picture changes dramatically.

The operating return is 26.8%. Not 11.1%.

The gap - 15.7 percentage points - is entirely the cost of acquisition debt. Dorman borrowed to buy SuperATV and a new deal in 2025. The interest on that debt eats into net income, which is what the 11.1% measures. But the underlying operations are earning 27 cents on every dollar of tangible capital deployed.

Why does this matter? Because debt gets paid down. Dorman’s total debt has already dropped from $849M to $633M since the SuperATV peak. As it continues to decline, the interest cost shrinks and more of that 27% operating return flows through to shareholders. The equity-holder return is converging upward toward the operating return.

It’s like buying a rental property with a mortgage - the property earns 12% on its value, but after mortgage payments you pocket 5%. As you pay off the mortgage, your take-home rate climbs toward 12%.

The moat assessment

Where does the moat actually sit?

It’s not brand (nobody knows Dorman outside of mechanics). It’s not patents (they have 500+, but the moat isn’t a patent wall). It’s not network effects. It’s a process advantage with three layers:

Speed. Dorman identifies failure modes, reverse-engineers a fix, and launches before anyone else. 1,659 “new to aftermarket” parts last year. By the time competitors copy, Dorman has moved to the next failure mode. The moat resets constantly - it’s a treadmill, not a fortress.

Complexity. Modern cars are stuffed with electronic modules - transmission controllers, engine computers, electronic steering racks. Reverse-engineering these requires decoding proprietary software. Dorman has 15 years of accumulated capability here. A Chinese generic manufacturer can copy a brake caliper. They can’t copy a transmission control module. And every year, the electronic content per vehicle increases. The barrier gets higher over time, not lower.

Scale. 138,000 SKUs. Distributors like AutoZone want one supplier who covers the catalog, not 50 vendors. Once you’re in the system at that scale, you don’t get ripped out. And when 21% of your competitors are in financial distress (per Lazard 2025), your 14% EBIT margins let you absorb the pricing pressure that bankrupts the 5%-margin players. You get their shelf space.

None of these alone is a wide moat. Together, they create a narrow-to-moderate moat that strengthens as the vehicle fleet ages and grows more complex. That’s the quality case.

The contrast that made it click

You still can feel that I’m sour from my Nike misjudgement. I tore it down last week and I am still digesting this position.

Nike earns less today than it did in 2015. It deployed $6.9 billion of incremental capital over a decade and generated negative $54 million of incremental earnings. The entire capital increase came from debt that funded share buybacks - not a single dollar went into productive reinvestment that grew the business.

Dorman is doing the opposite. It reinvests most of its earnings, earns 11% on that reinvestment (27% on an operating basis), and the business keeps growing. The trajectory is up, not down.

One is a compounder. The other is a cash machine running on fumes, returning money it doesn’t really have.

I own both. Draw your own conclusions about which one I’m more comfortable with.

What I paid and what I think it’s worth

I bought 50 shares at $100.19 during the early April sell-off. The stock was trading below my 30% margin of safety level for the first time.

The DCF model - built segment by segment, stress-tested with two NWC scenarios, cross-checked against a March version that arrived at the same number via different assumptions - says fair value is $154 per share.

That means I bought at 35% below fair value. In my framework, that’s comfortable. Not euphoric, not skinny - comfortable.

At the current price of $110, the stock is still 28% below fair value. The margin of safety hasn’t evaporated. It’s narrowed, but it’s there.

Key model assumptions:

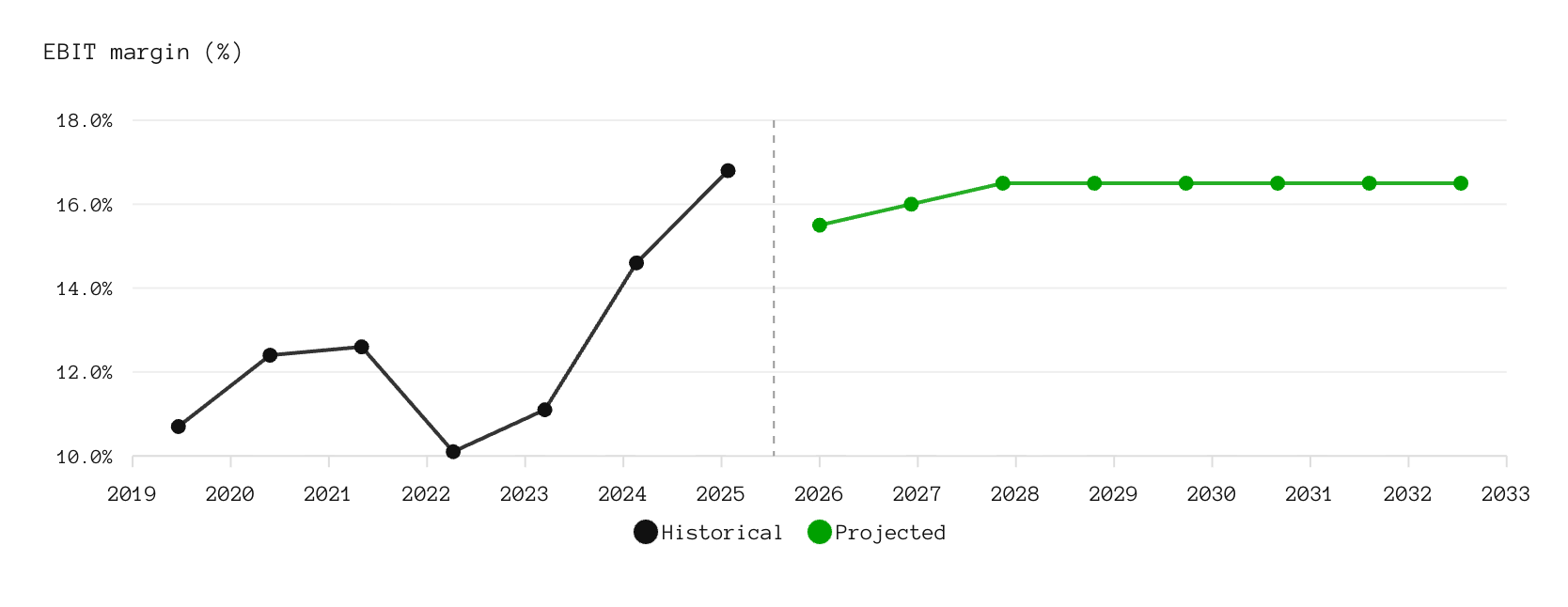

Revenue growth: 7-9% (management’s 2026 guide; I use 7%)

EBIT margin: 15.5% near-term (tariff drag), recovering to 16.5% steady state

WACC: 8.72%

Terminal growth: 2.5%

The model is conservative by design. It assumes margins stay below the pre-acquisition 17-20% range.

If margins recover to 18%, fair value moves to $175+. I’m not modeling that because I haven’t seen it yet.

The risks I’m watching

Customer concentration. AutoZone, O’Reilly, and Advance Auto Parts together account for a significant chunk of revenue. If Advance Auto goes bankrupt (it’s struggling), Dorman loses a customer but likely picks up the volume through other channels - mechanics still need parts. The bigger risk is pricing pressure from consolidated customers.

Tariffs. Dorman sources about 38% from China (down from 70% a few years ago). Management has been diversifying aggressively, but a Section 232 tariff at 25% on aftermarket parts would compress margins by 1-2 percentage points. This is already in my model.

The SuperATV question. Dorman bought a powersports company (UTVs, ATVs) that’s 13% of revenue and carries lower margins. This is an adjacency move - auto aftermarket company branching into recreational vehicles. Adjacency diversification is a yellow flag in the ROIIC framework. It suggests core auto runway might be narrower than management says. I’m watching whether SuperATV margins converge upward or stay as a permanent drag.

Boring doesn’t mean safe. The stock dropped 30% from its 2025 highs before I bought it. It can do that again. Dorman is illiquid by large-cap standards - a $5.5 billion market cap with moderate trading volume. It moves fast in both directions when the market gets nervous.

Why this matters beyond one stock

I started this portfolio last year, and the most important lesson so far is that my instincts about what makes a good investment were exactly backwards.

I was drawn to the names with the stories. Nike - iconic brand, turnaround, new CEO. Lululemon - premium athletic wear, loyal customers, international expansion. On Running - the hot shoe brand that everyone’s wearing. These names selling at a discount were looking like slam-dunks.

Every one of those “exciting” positions now is deeply underwater. I know it’s too early to tell, but the boring one - the one that sells exhaust manifolds and window motors - is the one actually making money.

This isn’t a coincidence. Boring businesses often compound because nobody’s paying a premium for the story. There’s no narrative to inflate the multiple. No influencer wearing Dorman brake calipers on Instagram. The stock trades on cash flow and earnings growth, not on vibes.

The ROIIC framework made this visible in a way I couldn’t see before. Nike has a famous brand and negative incremental returns. Dorman has no brand recognition outside of auto mechanics and earns 11% on every dollar it reinvests. The framework doesn’t care about your feelings. It measures capital efficiency.

I’m not selling Nike or the other positions - each has its own thesis and timeline. But if I’m being honest about where my conviction is highest, it’s in the company that makes car door handles.

Chuyka check

My gut says this is the kind of stock you buy and forget about for five years. The business doesn’t need a turnaround, doesn’t need a new CEO, doesn’t need China to cooperate, doesn’t need interest rates to drop. It needs cars to keep getting older. They will.

I am much more comfortable holding this position than many others in my portfolio. And if fundamentals stay strong I am happy holding it for years to come even if bargain price keeps persisting.

The model says it’s worth $154. My gut says the model is conservative. The fleet keeps aging. The electronics keep getting more complex. The catalog keeps growing.

Sometimes boring is the best thing you can own.

50 shares of DORM at $100.19 average cost. Current price ~$110. Fair value estimate $154. This is not investment advice. Think for yourself. Don’t trust online experts.

Trust your chuyka. Don’t let FOMO eat you alive.