Down 9% and Writing About It

My portfolio is down $5,200 this year. Every equity position is red. The best performer is a cash ETF that returned eighteen cents per share.

This is the first post on this Substack. Most people would wait for a winning streak to launch an investing newsletter. Show up with a track record, some screenshots of green numbers, a story about how they saw the bottom coming.

I’m a different beast. Down 9% YTD, holding six losing positions and a pile of cash, watching the market grind lower while oil trades above $100 and the Fed sits on its hands.

But here’s where I came from, where I am, and where this is going.

The passive decade

I started investing in 2014. My first trade was buying one share of Tesla and selling it eight minutes later. I didn’t know what I was doing, but I knew I wanted to learn.

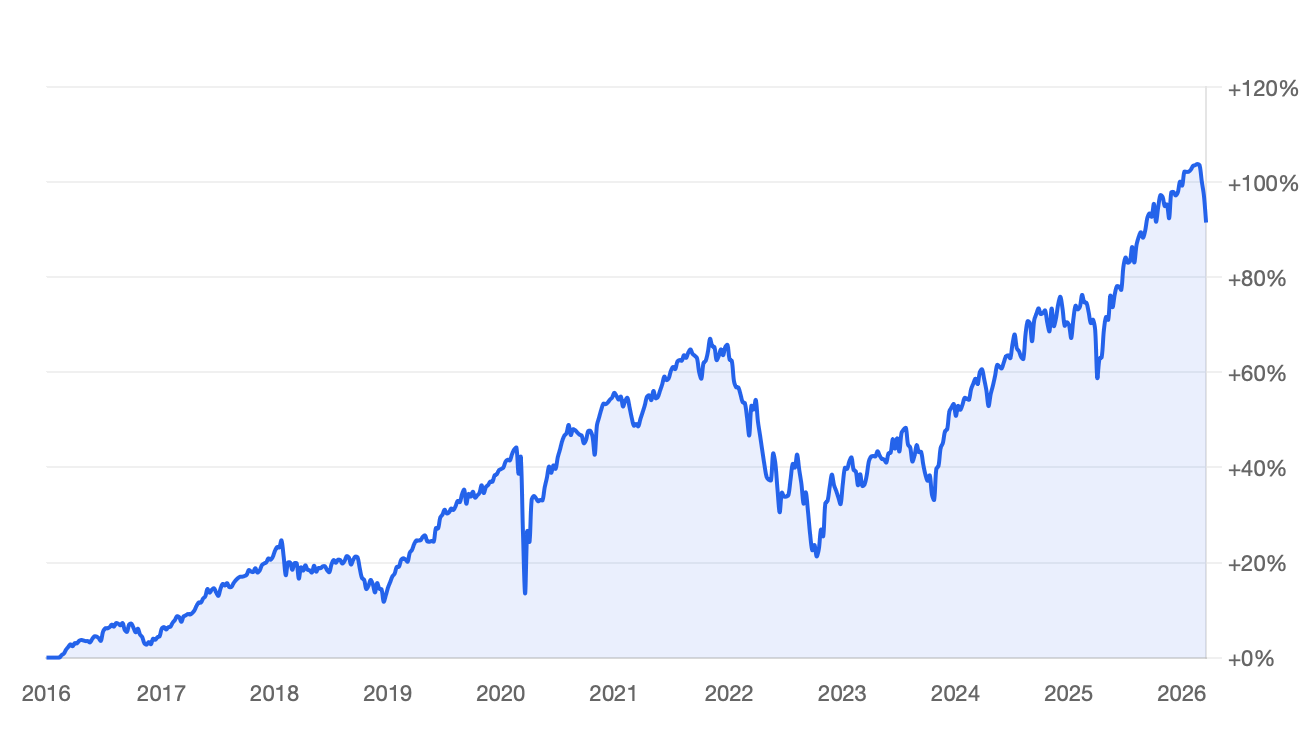

For the first couple of years I studied value investing. Intrinsic value, margin of safety, the whole Buffett and Graham reading list. I ran a blog about it in Russian. I had opinions about stocks I barely understood. Then life happened - career got demanding, I was working 12-hour shifts on oil rigs in Iraq, and I quietly switched to passive indexing. Meb Faber’s global asset allocation. Five ETFs: IVV, IEFA, VCLT, VGLT, PCY. Set it and rebalance once a year.

I ran that portfolio for a decade. It compounded at over 7% annually - decent, not spectacular. Most of that came from the S&P 500 carrying the rest. The international diversification, the bond allocation, the carefully balanced global exposure - all of it underperformed a simple 60/40 btw for most of the years, except when it beat S&P500 in 2025. I’ve achieved my goals of financial security and now it keeps running.

The biggest lesson from ten years of passive investing wasn’t about asset allocation. It was this: sitting still is the hardest thing in investing. Not selling during drawdowns. Not chasing what’s working. Not tinkering with something that’s fine. That discipline became the foundation for everything that came after.

The itch that wouldn’t go away

Somewhere around year seven or eight, the value investing itch came back. I’d been building data science skills through Yandex’s program, applying AI to problems in oil and gas at work, and I kept thinking: the tools have changed. What used to require a Bloomberg terminal and a team of analysts - pulling financial statements, building DCF models, screening for quality factors, reading earnings calls - a single person with the right setup can now do all of that.

Not better than a professional analyst. But good enough to make an informed bet. And that’s all value investing is - an informed bet with a margin of safety.

So in early 2025 I carved out $55,000 more from oil and gas money, opened a separate brokerage account, and started building positions. One stock at a time. Full transparency - every entry price, every share count, every P&L published in real time. (Now there is a Russian version of live tracking on my blog, but I will add an English one soon.) The passive portfolio stays. This is the experiment running alongside it.

The rules of the experiment

The philosophy is simple. Simple doesn’t mean easy.

Buy businesses, not tickers. I want to understand what a company does, how it makes money, and why it will keep making money five years from now. If I can’t explain it clearly, I don’t own it.

Value is the only reason to buy. I build a DCF model for every position. Full FCFF projection, explicit assumptions, terminal value with a sanity check on the implied multiple. The model gives me a fair value. I only buy below it - ideally at a 30-50% discount. No exceptions for “great company, fair price.” If the math doesn’t work, I wait.

Cash is not a failure. Half my portfolio is in SGOV right now. That’s not indecision - valuations are rich, and I’d rather hold dollars than overpay for a narrative. The ability to act during a selloff is an asset. Most investors are fully deployed when the best opportunities show up. I’d rather miss a rally than catch a falling knife without dry powder.

Show the work. Every stock gets a published deep dive with the full model. Not just “my fair value is $X” but every assumption behind it - revenue growth, margins, capex, WACC, terminal growth rate. You can disagree with any input and rebuild the model yourself. That’s the point.

Document mistakes. When I’m wrong - and I will be wrong - the losing trades stay on the record with the original thesis next to them. No deleting posts, no quiet exits. The process matters more than any single outcome.

Where things stand right now

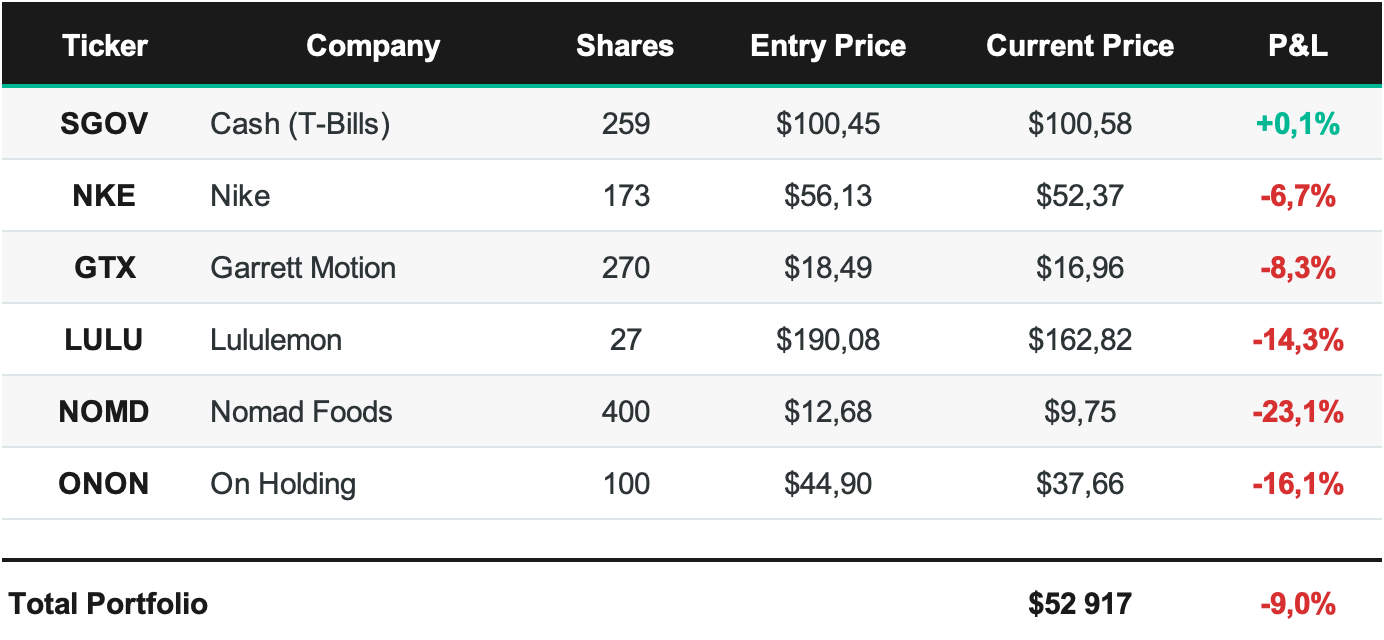

Let me show you what honesty looks like. Here’s the portfolio as of March 20, 2026:

Total portfolio value: $52,917. Down from $55,000 starting capital. YTD return: -8.95%.

Every single equity position is red. SGOV - the cash proxy - is the only thing in the green, and barely. The unrealized loss across the equity book is -$3,661.

This is what value investing looks like in practice. You buy stocks the market hates. Then the market keeps hating them. You sit there, check the thesis, and either add more or wait. The thesis on each of these names hasn’t changed. The prices have. That’s the difference between price and value, and being comfortable with that gap is the entire game.

Quick thesis summary on each:

NKE - Nike at $52, trading near a 52-week low. The market is pricing in a rough transition under new CEO Elliott Hill. I think the brand is too strong to stay here. March 31 earnings will be the next data point.

GTX - Garrett Motion, a turbocharger manufacturer spun off from Honeywell. Fair value per my DCF is $41. At $17 the market is pricing in permanent ICE decline. I disagree.

LULU - Lululemon post-earnings. The product quality is real - I own their stuff and it lasts years. At $163 it’s priced like a broken growth story. I think margins recover.

NOMD - Nomad Foods, European frozen food. Boring business, beaten down by a shelf filing overhang. Trading at 7x earnings for a company with stable cash flows.

ONON - On Holding. Best-in-class growth in athletic footwear. At $38 after a guidance miss, it’s the most expensive name I own and the one I have least conviction on. Minimum position size.

Started building that set of outcasts last year. It went well, until it didn’t.

Not one of these is a crowd favourite right now. That’s by design.

The plan from here

This is what Chuyka will be:

Stock deep dives - full analysis with DCF model assumptions. When I buy something, you’ll know exactly why, with every assumption laid out for you to challenge.

Portfolio updates - real numbers, real P&L, no hiding. When positions go against me, you’ll see it happen in real time. When I add or sell, you’ll know the reasoning right as I execute.

Process posts - how I source ideas (tracking superinvestor 13F filings, sifting through 52 week lows, mostly), how I read earnings calls, how I build models. The unsexy infrastructure of doing this alone.

I publish when I have something worth your time. Not on a schedule.

I’ve been writing about investing in Russian for over a decade. But I’ve been missing something important - the conversation. Thoughtful pushback. Someone saying “your WACC is too low” or “you’re ignoring the competitive threat from X.” That kind of discussion is how investing logic sharpens. Writing in English opens that door.

If you’re a value investor, an aspiring one, or just someone who wants to see what this process actually looks like with real money on the line - stick around.

If you’re here for hot takes and trade signals, this isn’t the place. I bought Nomad Foods. I hold 50% cash. Nothing about what I do is exciting. But I think it’s right.

Trust your chuyka. Don’t let FOMO eat you alive.

Not an investment advice. Think for yourself. Don’t trust online experts.