Garrett Motion (GTX): Turbos, Bankruptcy, and a Bet That Engines Don't Die

It's not just shoes and frozen veggies now.

Thanks for taking interest in my Substack. It’s a cold start, and we already have 2 subscribers, which is awesome. A warm welcome to Franek and cthunster for signing up. Much appreciated!

Before we continue, I would love if you subscribed using button below. I am looking for a thoughtful conversation and push-back on my positions. I am 9% down YTD and clearly something is not working. Your feedback is very important. Never thought that transition from passive to active investing would be such a rollercoaster.

Now let’s get into one of the more recent additions. I’ve bought 270 shares of GTX for $18.49 - it is now trading at around $17 amid the market sell-off. An opportunity to increase the position? Let’s test the thesis.

The bigger turbo

When I was younger I was into time attack. You take your car to a track and try to set the fastest lap in your class. I had a Mitsubishi Evolution X. Great car.

Since I couldn’t really drive, the main way to go faster was modifications. Intake, exhaust, ECU tune, cooling, tires, rip out half the interior. The basic minimum. The luxury maximum was always an engine rebuild - forged pistons, MOTEC brain, and a Garrett turbo kit.

I never got to the luxury maximum. Around the same time I got into investing. First I realized the best investment was in myself as a driver. Then I realized the best investment wasn’t in myself or the car - it was in the stock market. Sold everything. Here we are.

The dream of a bigger Garrett turbo and a louder exhaust had to go. But now I can afford to buy a piece of their company, trading under the ticker GTX.

What Garrett Motion does

Garrett Motion designs and manufactures turbochargers for passenger and commercial vehicles - gasoline and diesel. The company sells directly to OEMs: Volkswagen, BMW, Mercedes, Stellantis, plus Chinese automakers. A small share comes from aftermarket parts and automotive software.

Garrett is a former Honeywell division, spun off in 2018. In 2020 the company went through Chapter 11 bankruptcy - not from operational problems, but from asbestos liabilities inherited from Honeywell. Emerged in 2021 with a clean balance sheet, no legacy baggage.

Headquarters in Switzerland. 6,600 employees. Trades on NASDAQ. CEO Olivier Rabiller has been running the company since the spin-off.

Three major players in the turbocharger market: Garrett, BorgWarner, and what’s left of Honeywell’s turbo business. Effectively an oligopoly.

Why the stock is cheap

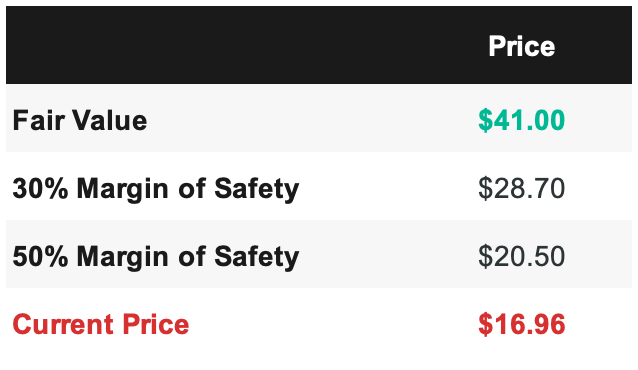

GTX traded at the time of original thesis at $18.23 against my DCF fair value of $41.00. P/FCF around 10x. EV/EBITDA at 8.6x. FCF yield of 9%. For a company that consistently generates $325-430 million in free cash flow, that’s not a lot.

The market is saying something like this: “Garrett is an ICE business. Electrification will kill it. Everything it earns today will slowly disappear.” That’s where the discount comes from.

52-week range: $7.01-$21.43. The stock is closer to the upper end, but still sits at the 50% margin of safety level from my valuation.

What management says

On the Q4 2025 earnings call, management explained the current situation:

Europe is weak. Light vehicle production hasn’t recovered to pre-pandemic levels (still -21%). Diesel keeps losing share in cities.

Commodity pass-through. Lower raw material prices mechanically reduce revenue by about 2% - margins aren’t affected.

Currency problems. EUR/USD and JPY swings cost about $34 million for the year.

China is the growth story. Win rate on new platforms above 50%. The bet is on PHEV/REEV - range-extender EVs where the combustion engine runs in a narrow RPM band and needs a high-performance turbo.

Fundamentals

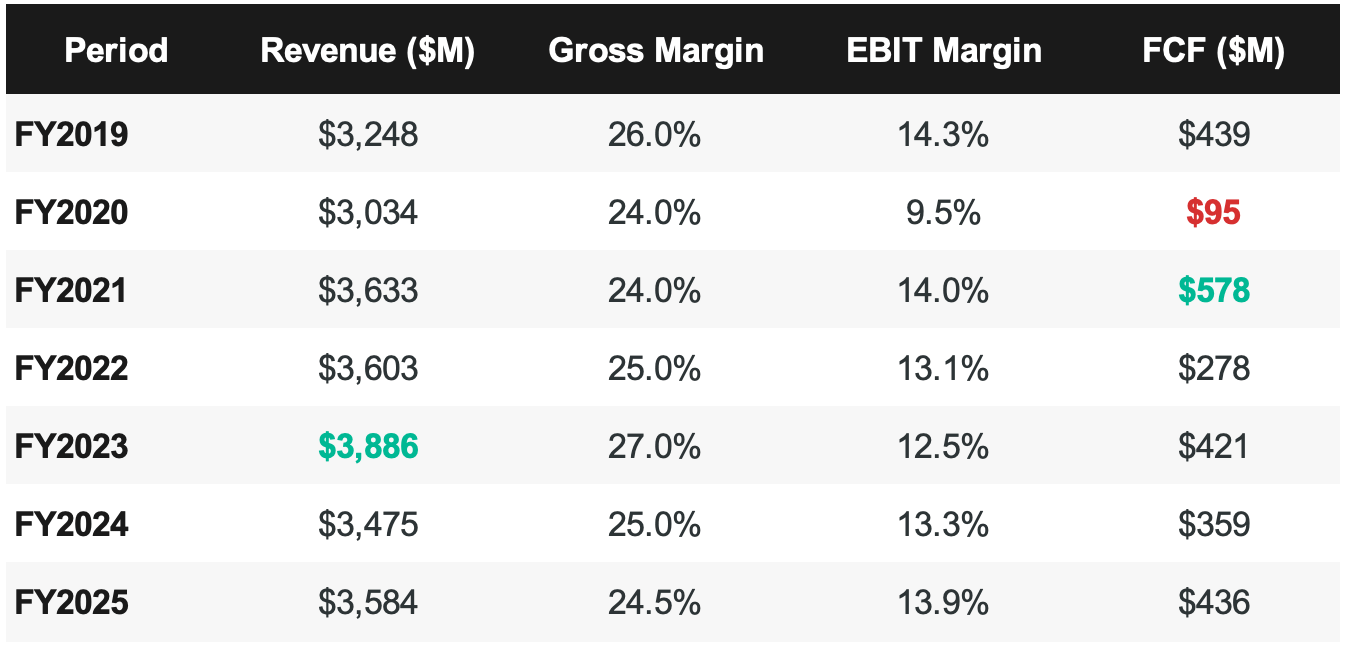

Revenue and margins

Revenue peaked around $3.9 billion in 2023 and has been gently declining. But EBIT margin holds steady at 13-14% - that’s 3x the sector average of 4.7% per Lazard’s 2025 Global Automotive Supplier Study. Gross margin stays in the 24-27% corridor across several cycles. Not a coincidence - structural pricing resilience.

FCF swings year to year because of working capital, but averages $300-440 million annually. For a company with a $3.5 billion market cap, that’s substantial.

Capital returns

This is where it gets interesting. Since emerging from bankruptcy, Garrett has been returning cash aggressively:

FY2023: $818 million in buybacks. More than FCF that year. Roughly 20%+ of the entire market cap repurchased in one year.

FY2024: $304 million

FY2025: ~$211 million + a new $250 million program announced for 2026

Dividend:

$0.28/share (1.5% yield)

Management targets converting 60% of EBITDA into capital returns. At TTM EBITDA of ~$595 million, that’s ~$357 million a year in buybacks and dividends. Promises match actions - that’s rare.

The flip side: aggressive buybacks pushed book equity into negative territory (~-$4/share). That’s not insolvency - cash generation is real - but P/B and ROE are now economically meaningless. Look at FCF yield and EV/EBITDA instead.

Balance sheet

Net debt: ~$1.4B

Net debt / EBITDA: 2.2x

Interest coverage: 4.7x

Current ratio: 0.97

Leverage is moderate. 2.2x on EBITDA isn’t aggressive for a business with stable FCF. But there’s not much buffer if volumes drop hard. A 25% fall in EBITDA pushes leverage to 3x - that gets uncomfortable.

Piotroski F-Score: 7/9

Strong. Fails on two signals: leverage ticked up slightly, current ratio sits just below 1.0. All profitability and operating efficiency signals are green.

Competitive moat

Narrow moat - engineering lock-in to the platform.

Turbocharger development is tied to a specific engine program. Certification takes 3-5 years. Once a supplier wins a platform, they stay on it for 8-12 years - the full lifecycle of that engine. OEMs don’t swap turbo suppliers mid-program.

But the moat doesn’t widen over time - it resets with each new engine generation. If ICE programs shrink, Garrett’s captive revenue pipeline shrinks with them.

One detail the market isn’t pricing in: Garrett is a consolidation beneficiary in a distressed sector. 20.6% of the auto supplier industry is already in financial distress per Lazard 2025. When weak turbo suppliers go bankrupt, their OEM content has to go somewhere. In an oligopolistic market (Garrett + BorgWarner), there aren’t many places for it to land. Garrett at 14% EBIT margin can absorb the pricing pressure that kills a competitor running at 5%.

Two catalysts that weaken the bear case

1. EU softened the ICE ban

In December 2025, the EU revised its 2035 target for banning combustion engines. Was: 100% emissions reduction (effectively a ban). Now: 90% reduction, with the remaining 10% offsettable through e-fuels, biofuels, and carbon credits.

The practical effect: OEMs that had frozen new ICE/hybrid program investments can now invest again. Every new engine program is a potential Garrett platform win for 8-12 years. The push for this change came from Germany, Italy, Hungary, and Poland - countries whose OEMs (VW, BMW, Mercedes, Stellantis) are Garrett’s core European customers.

2. China REEV is growing despite PHEV slowdown

Pure PHEVs in China have slowed (Q4 2025: -12% YoY). But REEV - range-extender EVs - is a different story: 640 thousand units in 2023 (+181% YoY), ~1.2 million in 2024 (+83%), forecast 3.2 million by 2030 (CAGR 17.1%).

Why this matters for Garrett: REEV generators run at a fixed optimal operating point - Miller/Atkinson cycle, narrow RPM band, maximum thermal efficiency (Chinese OEM engines hitting 46%). This demands more precise turbocharger engineering than a standard combustion engine. Commodity competitors lose here - plays directly into Garrett’s hands.

Li Auto tried to pivot to pure BEV - failed - and came back to REEV, targeting 550 thousand deliveries in 2026. Leapmotor is targeting 1 million units. Geely, BYD, Xiaomi, XPeng - all entering REEV. The trend is confirmed across multiple OEMs.

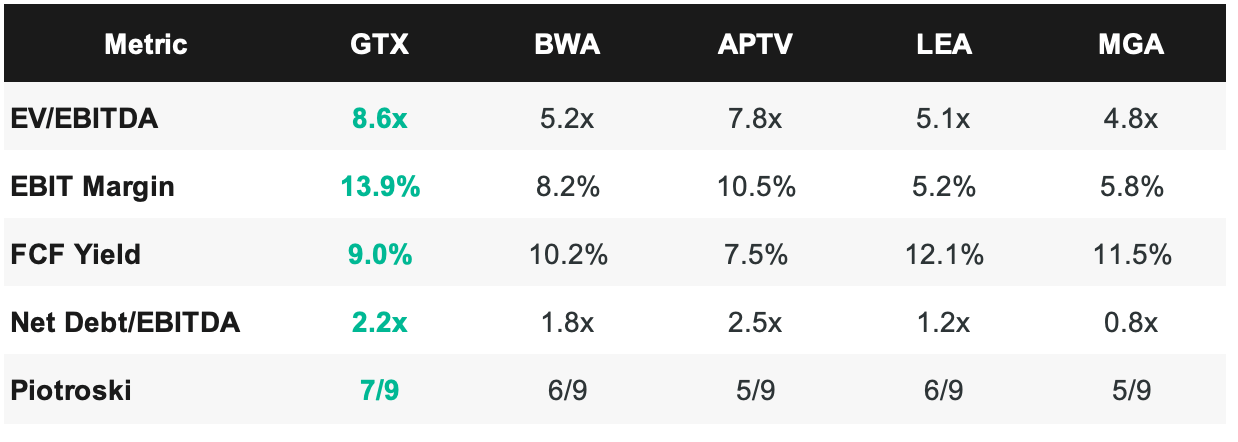

Peer comparison

Garrett stands out on margins - nearly double the nearest competitor. EV/EBITDA is higher, but that’s the premium for business quality. FCF yield is in line with the sector, but the quality of that cash flow is significantly better.

DCF valuation

Key inputs:

Revenue: $3,584M base, growing at +3% per year (linear)

EBIT margin: 14.0% (flat, at TTM level)

Tax rate: 21%

WACC: 6.45% (beta = 0.70, adjusted up from reported 0.376)

Terminal growth: 2.0%

Projection period: 8 years

At the current price, GTX trades below the 50% margin of safety level. The market is pricing in either a significantly worse revenue trajectory, or structurally lower margins, or a much higher discount rate. All three are possible - but all three at once?

Terminal value as % of EV: 72.2%. Near the 75% threshold but acceptable. Most of the value sits in the long-term franchise - turbo leadership plus potential EV products - not in near-term cash flows.

Risks

EV transition accelerates. The EU softened the target, but the drift toward electrification continues. If OEMs front-load their EV mix for CO2 compliance, revenue could decline 4-7% per year.

China REEV stalls. If the Chinese government pivots back to favouring pure BEVs, or if Li Auto and BYD start making turbochargers in-house, the thesis weakens.

Tariffs. Management flagged tariff risk on the Q4 2025 call. Cross-border manufacturing creates real exposure if trade wars escalate.

Leverage. At 2.2x net debt/EBITDA it’s manageable. A 25% drop in EBITDA and you’re at 3x - the safety cushion disappears.

Buybacks vs. debt. In FY2023 the company spent more on buybacks than it generated in FCF. The pace has slowed, but negative book equity is a fact. Financial flexibility is limited.

How to think about this

Garrett is not a “combustion engines forever” story. It’s a time-boxed bet on the 2025-2030 window. Over the next five years, ICE and hybrids hold roughly 60% of new vehicle sales per IEA, BloombergNEF, and S&P Global. In that window, Garrett collects cash, buys back shares, and builds new product lines - e-boosting, fuel cells, e-cooling for data centres.

The question isn’t “will ICE survive?” It will, at least until 2030. The question is: “will Garrett earn the right to compete after 2030?”

At 9% FCF yield and buybacks shrinking the share count every year, the hurdle rate for acceptable returns is very low. Even with stagnant revenue, the math works. If China REEV accelerates and the consolidation thesis plays out, the upside is significant.

I bought 270 shares of GTX at $18.49 in my active portfolio.

Chuyka Check

After all the numbers and all the models - here’s what sits with me. Garrett is the kind of stock that makes you feel slightly uncomfortable owning. The market narrative is clean and easy to understand: EVs will kill this business. And maybe they will. Eventually.

But “eventually” is doing a lot of heavy lifting in that sentence. The turbocharger industry isn’t shrinking tomorrow. It’s an oligopoly with real engineering barriers, and the China REEV angle is something most investors haven’t even looked at. The company throws off cash like it’s going out of style, and management is buying back stock at prices that my model says are half of fair value.

My chuyka says this is one of those situations where the market has priced in a death that’s 10 years away and forgotten about the 5 years of cash collection in between. I could be wrong. The EV timeline could compress. But at this price, I’m getting paid to wait and find out.

If you want to follow me and see if I am wrong or right in my assumptions - here is a field with a button for you :)

Trust your chuyka. Don’t let FOMO eat you alive.

Not an investment advice. Think for yourself. Don’t trust online experts.