Is it time to buy UBER?

From burning venture cash to FCF powerhouse with a moat

Last week I’ve finished most of the work required to launch backrunner, so now I am free to get back into my favourite activity - researching and finding new stocks to buy. Today we talk about how Uber suddenly became a value pick. As most of the stories with beaten stocks today - there is a big bad AI (or in this case AV) threat. But lets dive in and see if Uber is up to weather this storm and can come out on top?

What Uber actually is

Uber is a toll booth on movement. Somebody wants a ride, a burrito, or a pallet of freight moved. Somebody else has a car, a bike, or a truck. Uber stands in the middle, matches the two, and keeps a cut of every transaction. That is the whole business. The cut, what they call the take rate, runs around 27% blended.

Three pieces. Mobility is the rides business, the profit engine, roughly $30 billion of revenue and the highest margin. Delivery is Uber Eats plus grocery, the growth engine, growing bookings faster than Mobility and now solidly profitable. Freight is digital trucking brokerage, small, still losing a little money.

The interesting bit is the flywheel sitting on top. Uber One, the membership, hit 50 million members by Q1 2026 and those members now drive about half of all gross bookings. People who use both rides and Eats spend roughly three times more and stay around far longer than single-app users. And Uber acquires those cross-app customers almost for free, by promoting Eats inside the rides app and the other way round, at roughly half the cost of buying them through ads. Layered on that is an advertising business now running past $2 billion a year and growing about 50%, which is nearly pure margin and quietly lifts the take rate.

So the engine is volume times take rate, and the volume keeps climbing while the high-margin layers (ads, membership) push the cut higher. Good engine.

Why it is cheap

Uber fell from about $102 to near $70, roughly a 29% haircut, and bottomed near its 52-week low. During all that the operations accelerated. Q4 2025 had gross bookings up 22% and segment EBITDA up 35%. Q1 2026 had bookings up 25% and EBITDA up 33%. Those are not the numbers of a business in trouble.

The market re-rated Uber down on one fear: autonomous vehicles. Tesla launched an unsupervised robotaxi across the whole Austin metro on June 3, 2026, on its own app. Waymo runs its own app in most cities it operates. The bear story writes itself. The competition is gearing up to be tough. I’ll share some data on that below.

Still if self-driving cars become the supply, and they go straight to the consumer, who needs the middleman? The toll booth gets bypassed.

That is a real question. I will come back to it, because it is the question. But notice what the de-rate is and is not. It is multiple compression on a narrative about 2028 and beyond. It is not the current cash flow breaking. The cash flow, in fact, is the best it has ever been.

Bill Ackman is in

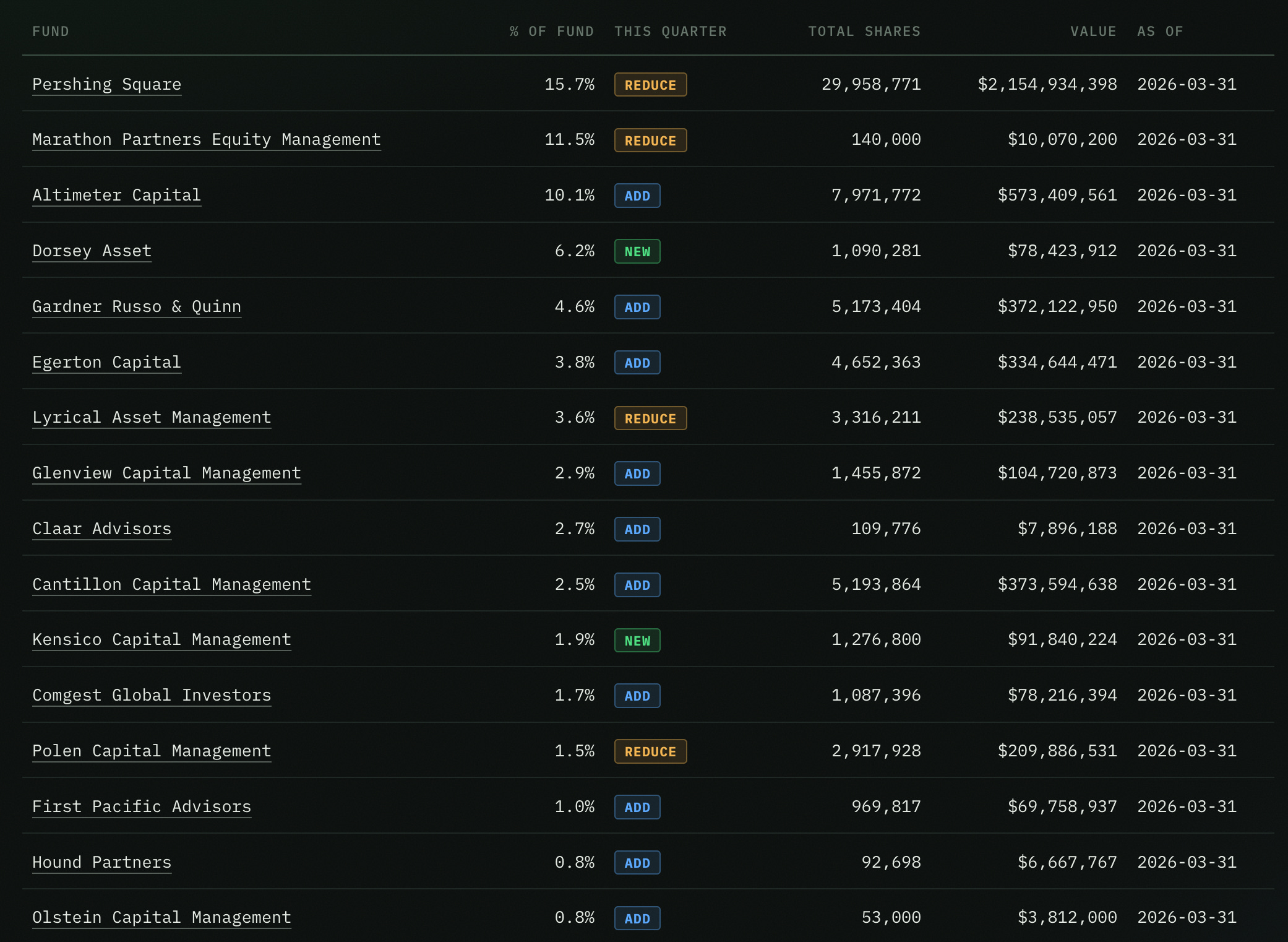

One more data point, for what it is worth. Courtesy of my handy backrunner.io fund universe.

In Q1 2026 the consensus starts to build around UBER in the professional money manager space.

First lets look into reductions.

Pershing is a slight trim of the position 15.9% reduced to 15.7% of fund. Marathon sold 7% of shares, probably to fund new positions and additions. They still have high conviction at 10% of the fund in UBER, but their total position is relatively small. Lyrical sold 6% of their position in a porftolio-wide reduction. Still 11th largest position of the fund which is on a less concentrated side.

Everyone else on the list added/bought. Across backrunner universe I see total of 3.2 million of shares positive buying delta to a total of $241 million additional conviction in Q1 alone.

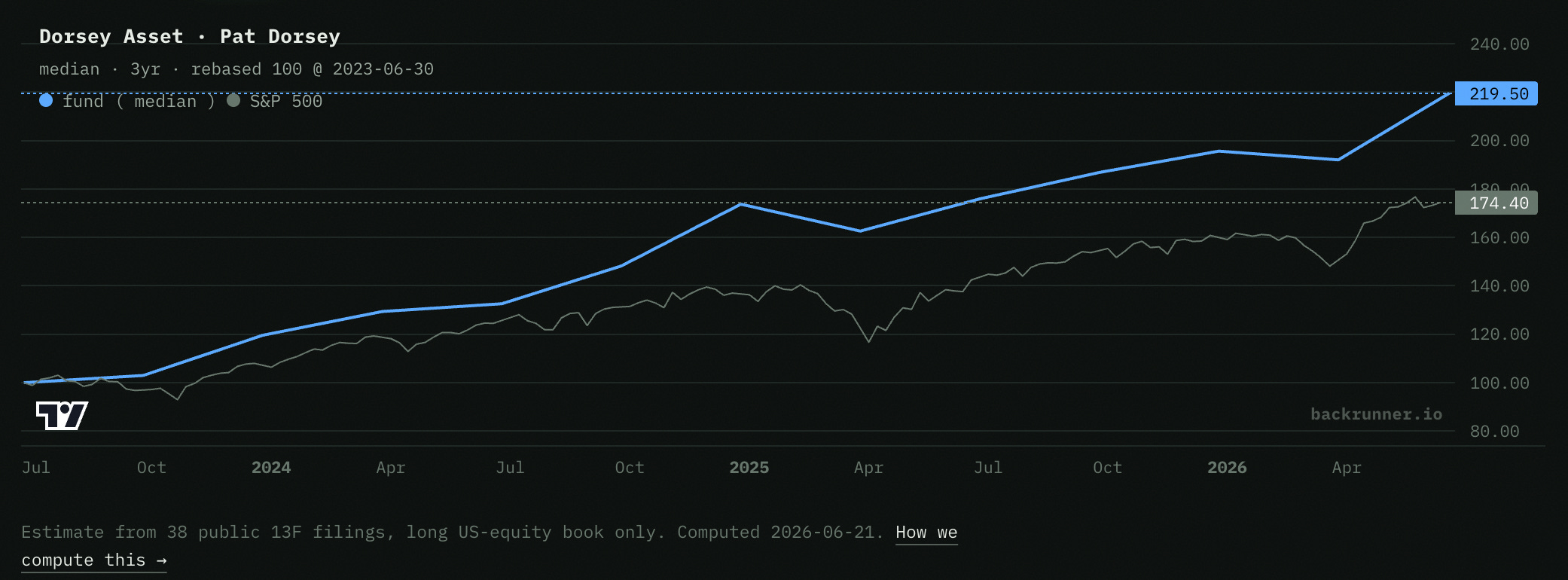

Pat Dorsey opened UBER as a 6% stake in 11 stock portfolio. And he has been on a decent run recently.

This is a rare new formed conviction signal which is alone a solid reason to look deeper into this.

Substack investors are in

There are a few substackers covering Uber.

Manu from Fundamentally Sound has a great piece on Uber. Is a shareholder and posts regular updates. He was one of the earliest among substackers I follow who spotted the potential.

Pete from Bulding Arks covers Uber very closely and is bullish on Uber. He mentioned that he holds it in his portfolio.

Quality Stocks had Uber as one of 12 stock picks for 2026. Read well with later Q1 update on performance.

The fundamentals: an engine that just switched on

For most of its life Uber lit money on fire. The venture years (2018 to 2022) were a subsidy machine, burning billions to buy growth.

Then it flipped.

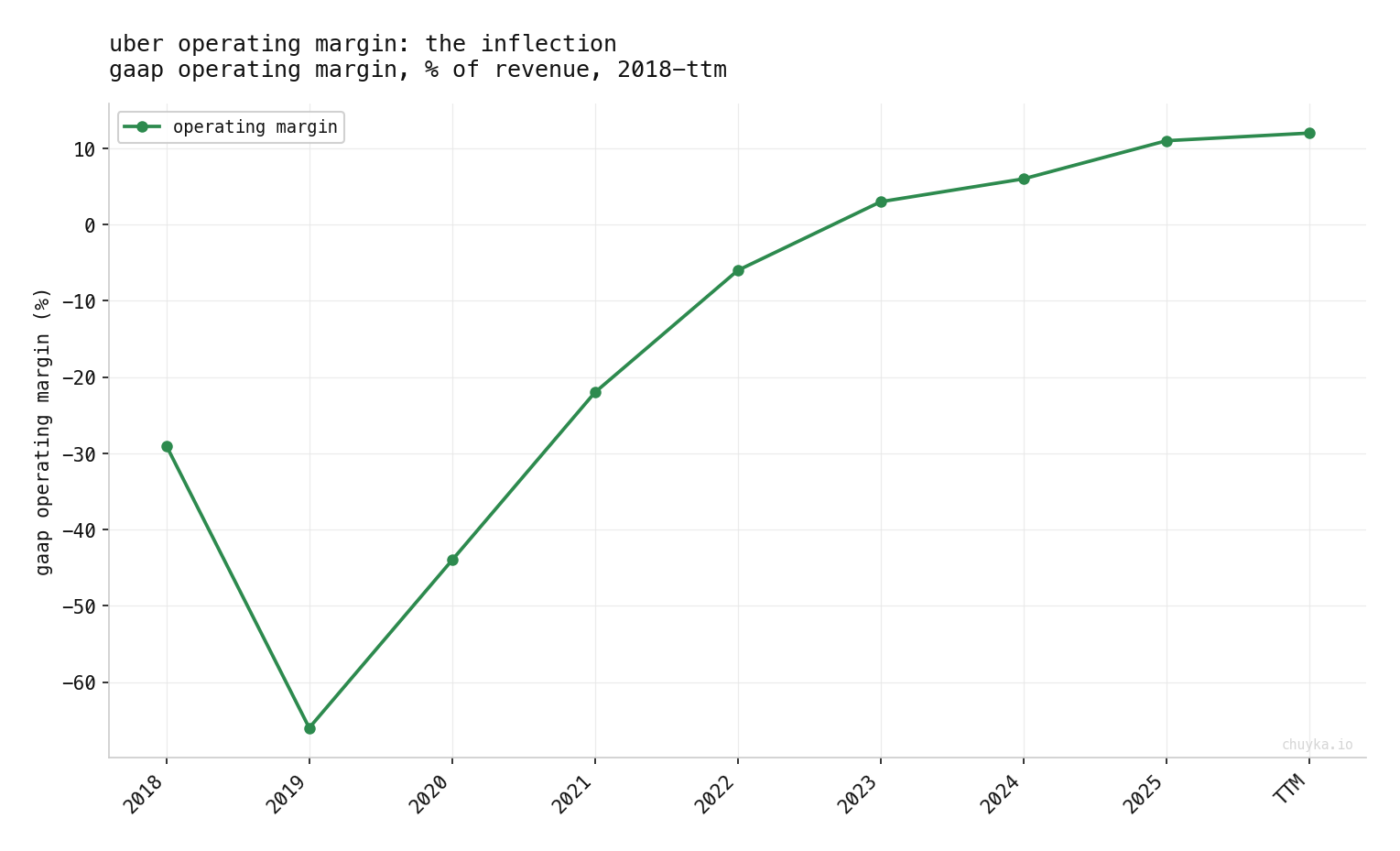

Operating margin went from minus 29% in 2018 to plus 12% on a trailing basis. It crossed zero in 2023 and has compounded since. And the cash followed.

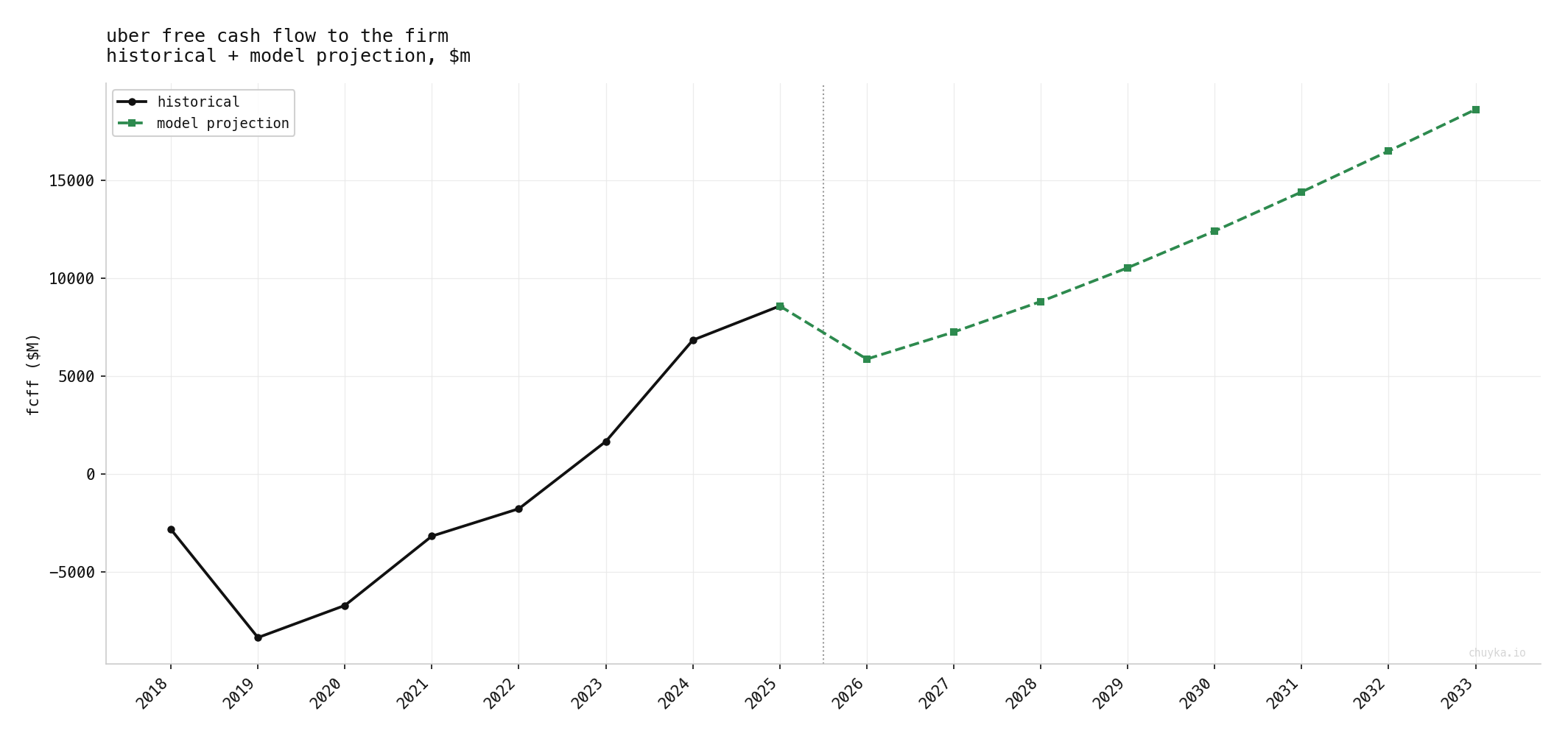

Free cash flow turned positive in 2022, then ramped to roughly $9.8 billion in 2025. And it is clean cash. The accruals are negative, meaning cash runs ahead of reported earnings, the opposite of the warning sign you look for.

Uber is now also retiring shares, after years of printing them to fund losses, buying back around half of its free cash flow and shrinking the count about 3.5% a year.

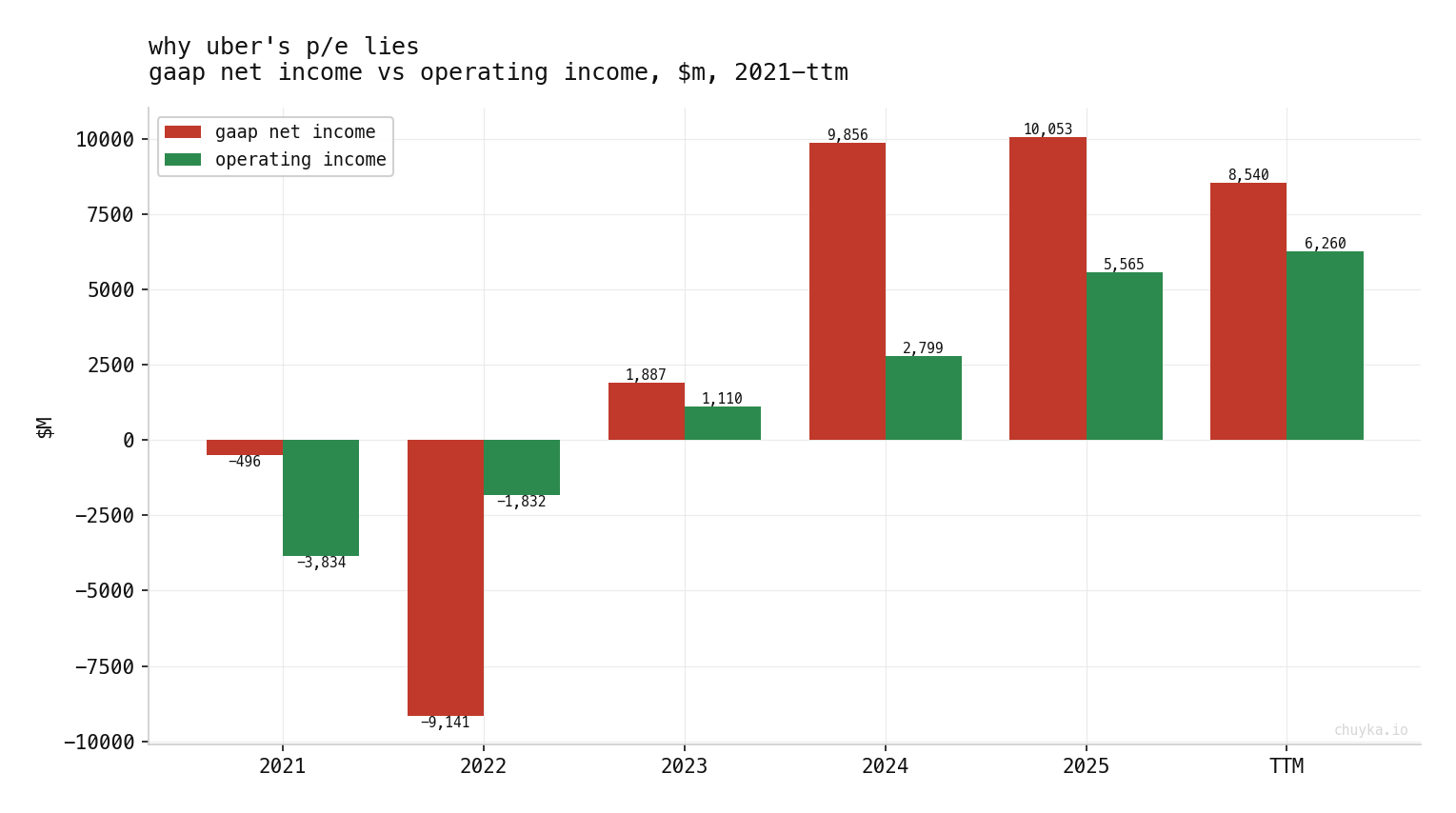

Now the part that trips most people up. If you pull up Uber’s P/E, it looks like a rather cheap tech stock at ~17x. Ignore it. The earnings number is junk.

Look at 2022. Operating income was minus $1.8 billion, a manageable loss. Reported net income was minus $9.1 billion. The extra $7 billion of “loss” was the paper writedown on Uber’s equity stakes (it owns chunks of Didi, Grab, Aurora and others), not anything operational. Then run it forward to 2024 and 2025, where net income is roughly double operating income. That gap is mostly a one-time tax benefit: Uber released about $6.4 billion of deferred-tax allowances in 2024 and another $5 billion in 2025, non-cash, never repeating.

Strip the tax releases and the equity marks and net income lands back near operating income, around $5 to $6 billion. Management knows this. In late 2025 it switched its headline profit metric away from net income toward adjusted operating income, which is a polite way of admitting the GAAP number overstates the real thing.

So UBER is not cheap on P/E. The real P/E is somewhere around 30. The honest lenses are free cash flow and the operating line. On those, the business is inflecting hard and generating real money.

The moat, and where it ranks

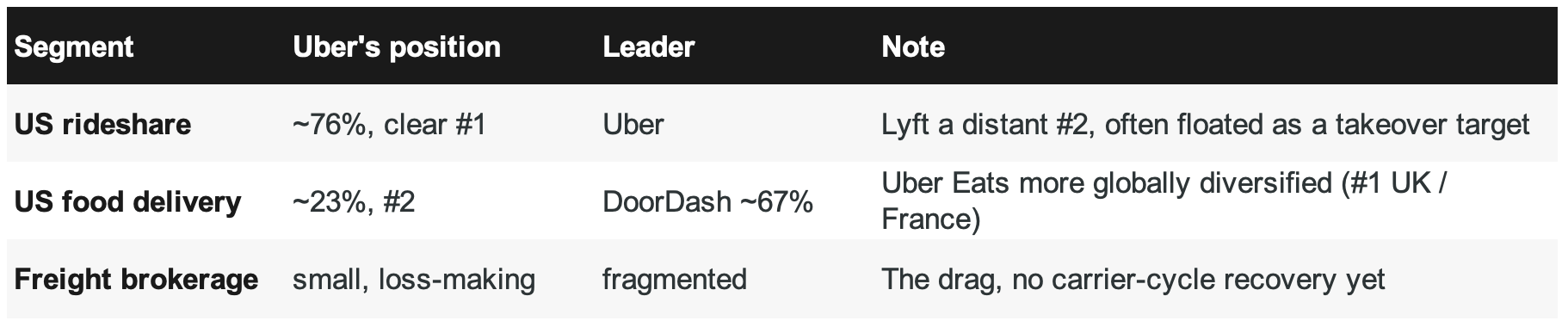

Two-sided networks are among the best business models there are. More drivers mean shorter waits, which means more riders, which means more drivers. Density compounds. Uber One adds a switching cost on the consumer side. In US rideshare, Uber holds about 76% share, with Lyft a distant, sub-scale second.

So the moat is real. But I want to be honest about its limits, because this matters for how much margin of safety I demand.

Apart from Uber One providing some sort of stickiness - switching costs are low. The same driver runs Uber and Lyft on two phones on the same dashboard. The same rider checks both apps for the cheaper fare. That caps pricing power and keeps the core service close to a commodity. Uber’s edge is liquidity and convenience, which is genuine, but it is not a toll nobody can route around.

Put it on a spectrum. A card network like Visa, or a credit-ratings business like S&P Global, is near-impossible to substitute.

Uber is a notch below that. It is a strong network, but a contestable one, and it carries a question those toll-takers simply do not have: a live technology threat that could rewire its supply side.

The right comparison set is other marketplaces, DoorDash, Airbnb, Booking, MercadoLibre, not the payment duopolies. That placement is exactly why I want a wider discount here than I would accept for a cleaner compounder I might consider with no MoS at all.

And we also covered another moat - vs AV disruption, but again, I think it is robust enough and we will cover it below.

Can the cash flow survive?

A value pick is not just cheap. It has to be durable. So: what could break this cash machine?

Ordinary competition and the cycle. Not much of a worry. The growth is volume-led, not price-led, trips up about 20% while price per trip is roughly flat. Penetration is still low, only around 10% of adults in Uber’s top markets use it monthly, so the runway is long. It is discretionary spending, so a real consumer recession would slow it, but rides and cheap meals are sticky habits, not luxury splurges. The one cost lever I keep an eye on is insurance, Uber’s single biggest variable cost, where it self-insures and carries large reserves; a bad run of claims hits the P&L directly.

The balance sheet. Fine. Net debt is around one times EBITDA, there is no dividend commitment, and the company is buying back stock rather than stretching. Nothing here forces a bad decision in a downturn.

Autonomous vehicles. This is the one that matters, and it deserves its own section.

The AV question

Everything above is favourable. Cheap, cash-generative, growing, a real network. The entire thesis comes down to one unresolved question, and the same facts read as both bull and bear.

The bull case

AV is just another kind of supply Uber plugs into its network.

Uber sold its own self-driving unit years ago and now positions as the demand-and-fleet-operations layer.

It says Waymo cars routed through Uber’s app in Austin and Atlanta run higher utilization and faster pickups than they do standalone, and autonomous trips on Uber grew about 10x year over year in Q1 2026.

I’d say that this is the most important overlooked aspect of Uber. It’s not just an app. It is everything that they’ve learned along the way to the top of the market. That is hard to replicate without burning through tons of cash. And if you are trying to build that capability while hammering CAPEX on your own fleet - that’s a steep climb.

Balancing a mixed human-and-robot fleet, and handling the unglamorous fleet ops (charging, cleaning, maintenance), is hard for a single carmaker to do alone.

In this version Uber stays indispensable and AV is not a threat - is the upside.

The bear case

Tesla and Waymo run their own apps. If self-driving supply concentrates in a few players and they go direct to riders, they compress Uber’s take rate or skip it entirely. The toll booth gets bypassed.

But lets vibe on that for a minute. Humanless taxis seem to be the obvious endgame for the industry. If you look at consumer reports - once people try them - they start to prefer them to human-operated ones. But it’s not clear-cut.

For some users privacy aspect matters. I prefer not to talk to taxi drivers for example, rather linger in my own thought. Making a private call or having an honest deep conversation with your companion is a no go.

Safety is also a concern. Drivers in the lower tiers can drive aggressively or can behave unpredictably. No driver - no risk.

So to me, personally - there is no wonder why this mode of transportation is taking off.

But. Today robotaxis are 30% more expensive. And it is not clear if they can get cheaper in the long run. Right now Waymo is in the same venture state as Uber was 5 years ago - subsidising growth. There is a case can be made that robotaxis are structurally more expensive.

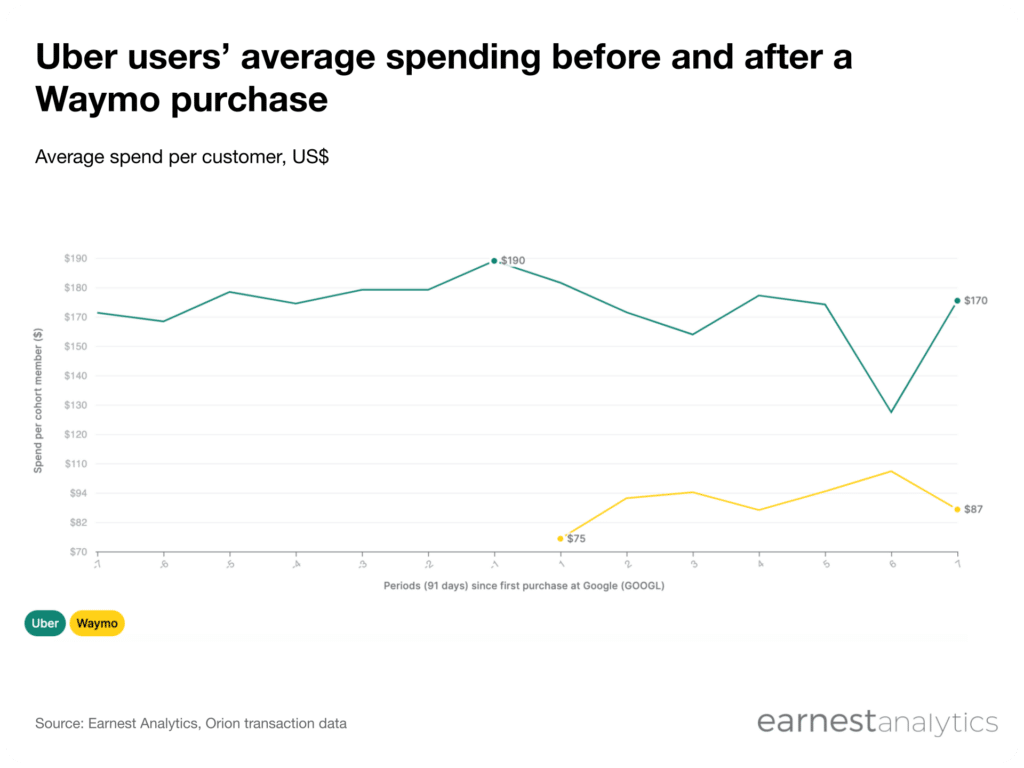

There is also a symbiotic relationship between AV providers and ride-hailing service in general. Robotaxis do not cannibalise the traditional service, but expand it.

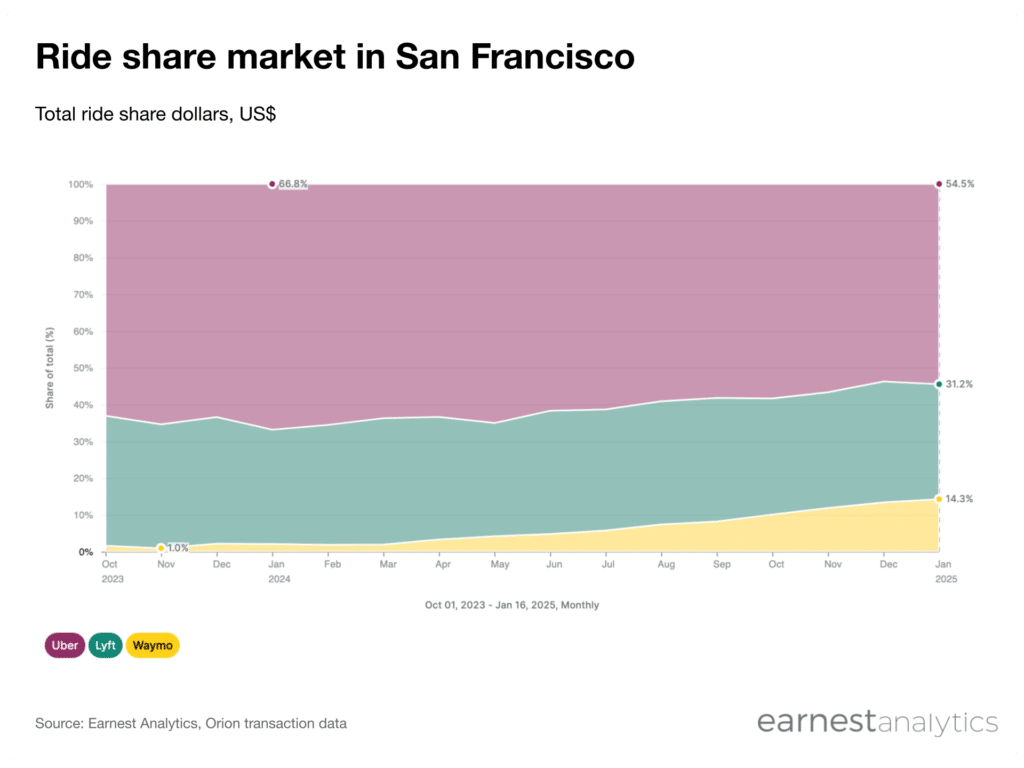

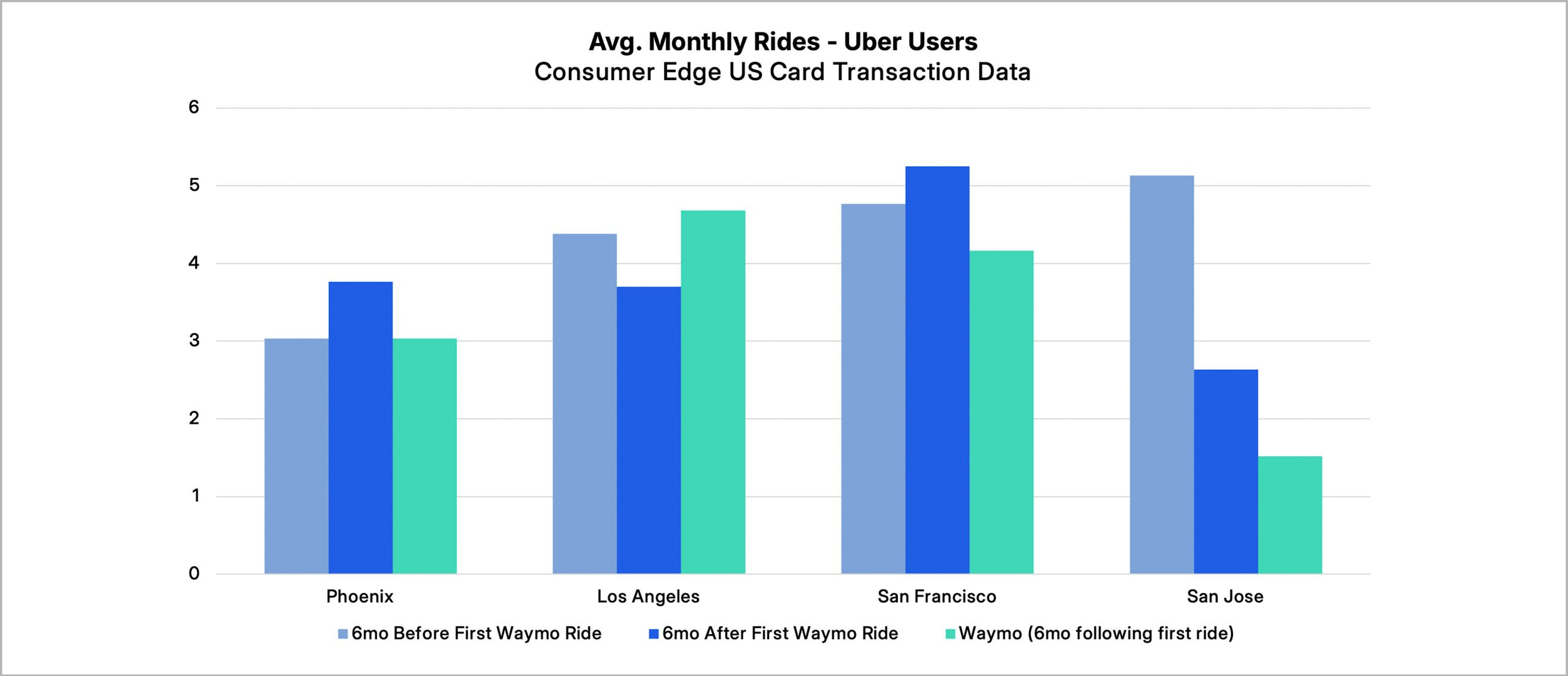

The Uber share got lower in cities where Waymo operates, true. But overall spending on transportation grew. And if the final model is Uber wiring Waymos through their app like they do in Austin and Atlanta - it’s a net win for Uber.

In Phoenix where hybrid model exists (both standalone app and Uber wiring exists) total rides for Uber increased after Waymo launch. In direct competitive markets (LA, SF and San Jose) results are mixed.

So the honest read: it’s too early to tell. Uber is now committing more than $10 billion to own AV supply directly (fleet deals, builder stakes, a 20,000-vehicle Nuro/Lucid arrangement).

This is the thing to track quarter by quarter: autonomous trips on Uber versus on first-party apps, whether the take rate holds in AV-heavy cities, and how fast the capex ramps.

UBER fair value

I built an FCFF discounted cash flow on the operating line, which routes around all that polluted net income. Revenue growing 15% fading to 7% over eight years, operating margin climbing from 13% toward 20% (still below the ~25% the segments already earn, so not a stretch), tax normalized to 22%, and a 8.94% discount rate. The terminal multiple works out to about 12x operating profit, not heroic.

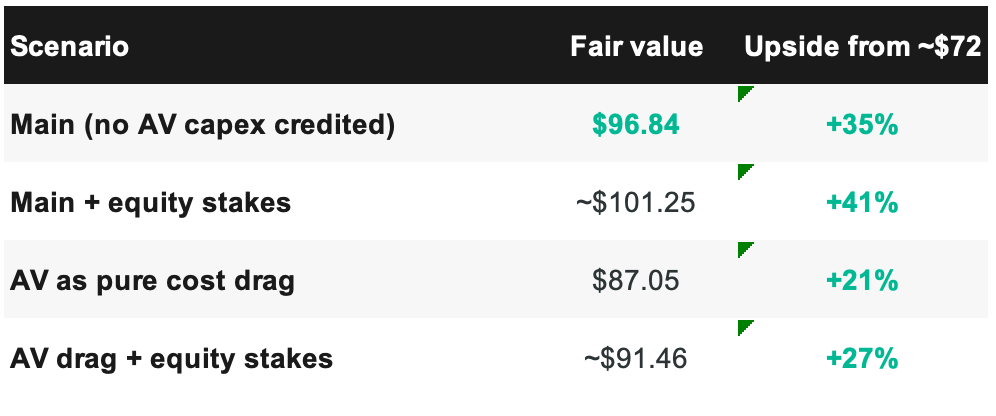

That fair value is deliberately conservative, on three counts. The 22% tax rate ignores that Uber pays almost no cash tax today on old losses, so it gives up a real near-term benefit. The model holds the share count flat, crediting nothing for the ~3.5%-a-year buyback. And it excludes the $9.35 billion of equity stakes Uber owns in other companies, which are real assets, worth about $4 a share.

Fold those in and the variants look like this:

Here is what I like about that bottom row. Even if I assume Uber spends $10 billion-plus on autonomous vehicles and earns nothing back, a deliberately punishing assumption, fair value is still around $87, comfortably above the price. The downside case is not a loss, it is a smaller win. That is the kind of asymmetry I am looking for.

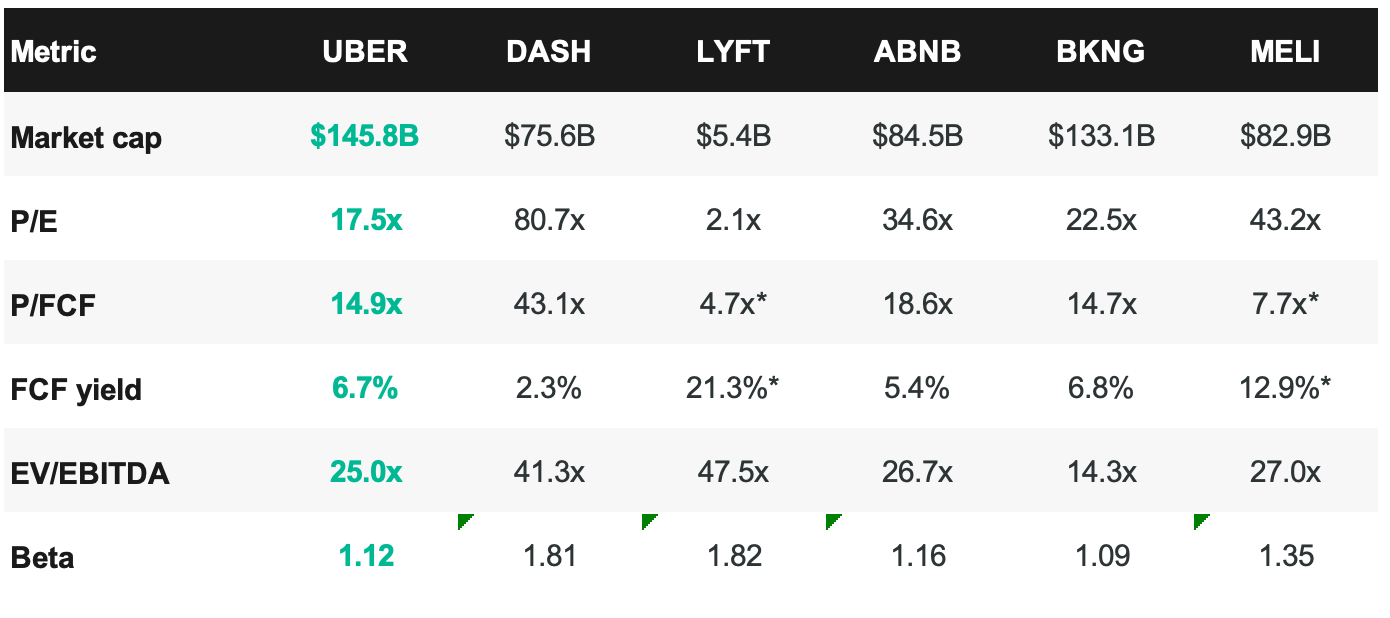

Against peers, the cheapness shows up clearly:

Among the genuinely profitable platform networks, Uber sits next to Booking as the cheapest on free cash, well below DoorDash and Airbnb, and it does it on the lowest beta of the group. Wall Street’s average target sits around $104 to $107, above my conservative $97. I am happy to be the more cautious number in the room.

The risks I actually worry about

AV disintermediation. Covered above. The thesis gate. If the take rate starts compressing in AV-heavy cities, I am wrong.

The capex pivot. The $10 billion-plus AV commitment is the asset-light story eroding in real time. If that spending scales faster than the cash flow can absorb, the clean FCF picture bends. Watch capex as a share of revenue.

Labour law. The US is largely settled. Europe is not: the EU Platform Work Directive must be written into national law by December 2026, and it carries a presumption that drivers are employees. Court rulings so far are split. A driver-reclassification ruling in a big market would hit the cost structure.

Earnings optics. Not a cash risk, but the equity-stake marks swing reported profit by over a billion dollars a quarter. It makes the headlines ugly and the comparison messy, and some investors will keep mistaking the GAAP number for the truth.

Multi-homing. The structural cap on pricing power. It is not going away.

Bottom line

So, is it time to buy Uber?

Almost. Not quite.

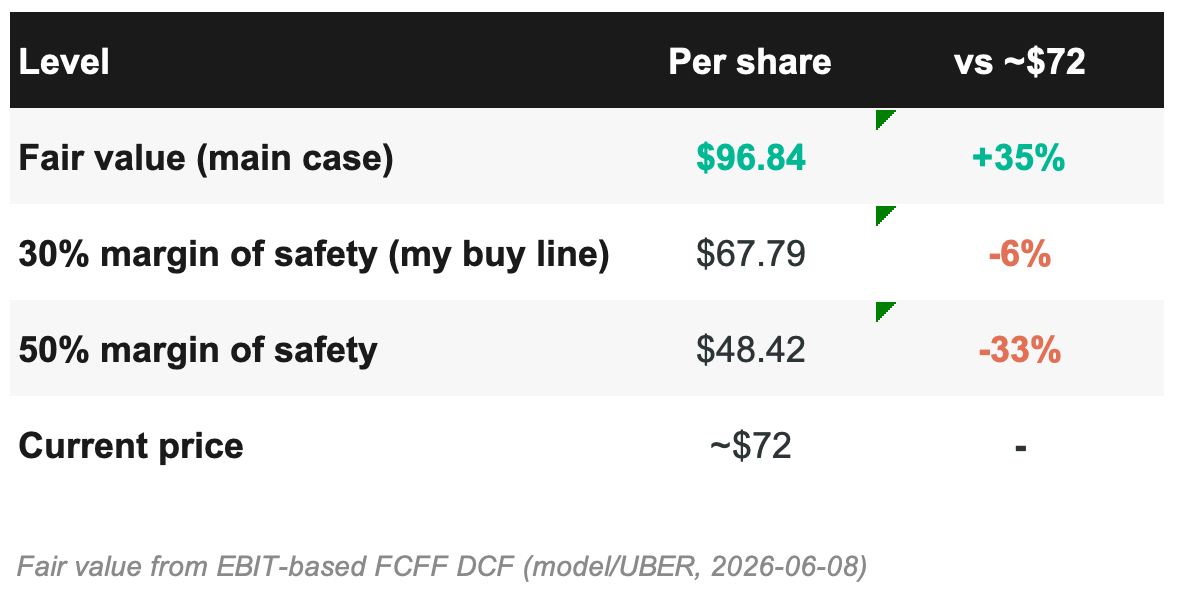

Here is the honest position: I do not own it. At around $72 the stock is about 6% above my buy line of $67.79, and roughly 35% below where I think it is worth.

That is close. It is the first genuinely cheap megacap I have looked at in a while, and it would diversify a book that leans heavily on consumer and apparel names. I want it.

But 6% above my line is still above my line. I set that 30% margin of safety precisely because the AV question is unresolved, and a network with low switching costs deserves a wider cushion than a clean toll-taker. Paying up 6% to chase it would be exactly the FOMO this newsletter is named against. So I wait. The trigger is $67.79, or a Q2 print in early August that either calms the AV fear or confirms the cash flow is holding through the capex pivot. A small dip, or one good quarter, and this moves from the watchlist into the portfolio.

Chuyka check

After all the math, my gut says the crowd is selling the wrong thing. They are pricing a 2028 robotaxi best case nightmare onto a 2026 cash machine that is compounding right in front of them. The network is the kind of thing that tends to survive transitions by absorbing them, and Uber spending $10 billion to own the threat tells me management would rather hedge than hope.

But the chuyka does not override the discipline. The AV question is genuinely open, not a fake bear narrative, and that is exactly why I want my full margin of safety rather than a partial one. The model says $97. The market says $72. My gut says the model is, if anything, conservative. And the same gut says: do not pay up six percent to feel clever. Wait for the pitch.

Position: None. Watching, with a buy trigger at $67.79 (30% below my $96.84 fair value estimate). Fair value range $87 to $101 across scenarios. Live peer data via FMP, June 2026. This is not investment advice. Think for yourself. Don’t trust online experts.

Trust your chuyka. Don’t let FOMO eat you alive.