I held Nike at $74. Now it's $44, down 40%. Turns out my model was garbage the whole time.

I rebuilt my Nike valuation from scratch. Fair value went from $77 to $38. $43 per share of delusion, dissected.

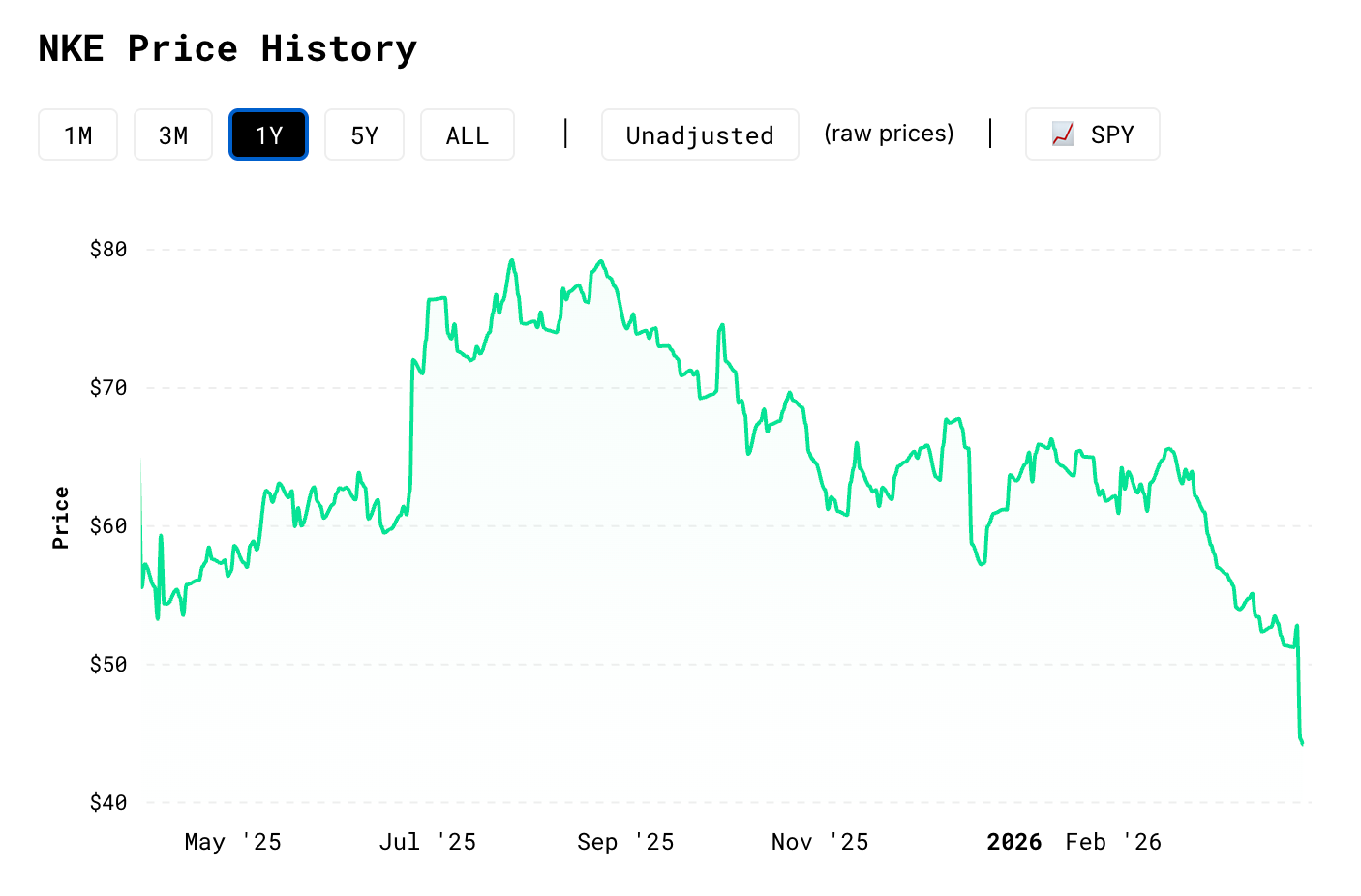

Six months ago I published an analysis of Nike on my Russian blog. I said the stock was worth $77. Did the whole DCF analysis thing. I bought at $56 per share and felt pretty good about it.

Go read it if you want. It’s in Russian, but the numbers are universal.

But the story went in a wild direction.

For a while, the market agreed with me. Nike ran to $74 - up 31% from my entry. I was sitting on $3,000 in profit, watching the thesis play out, feeling like a value investing god. Six months back into stock picking after a decade of index funds and already up 31% on my first high-conviction idea. Hard not to feel validated.

Then it went to $44.

I just rebuilt the model from scratch. New framework, proper assumptions, segment-level revenue, actual working capital math. New fair value came out at $38.

Not $77. Not even close. $38.

The stock currently trades around $44. I own 173 shares at a $56.13 cost basis. That’s roughly $2,000 in unrealized losses, or about -21% on the position. This mistake has a price tag, and I look at it every day in my portfolio.

This post is about the five specific mistakes that created a $43 gap between what I thought the company was worth and what it’s actually worth. Not hindsight. Every one of these errors existed when I built the original model and could have been caught then. I just didn’t know what to look for.

What the old model said

The bull case was straightforward. Nike has problems - everyone knows this. Failed DTC strategy, aging product lineup, new CEO cleaning up the mess. But the brand is iconic, free cash flow is healthy, and turnarounds at this scale tend to work eventually.

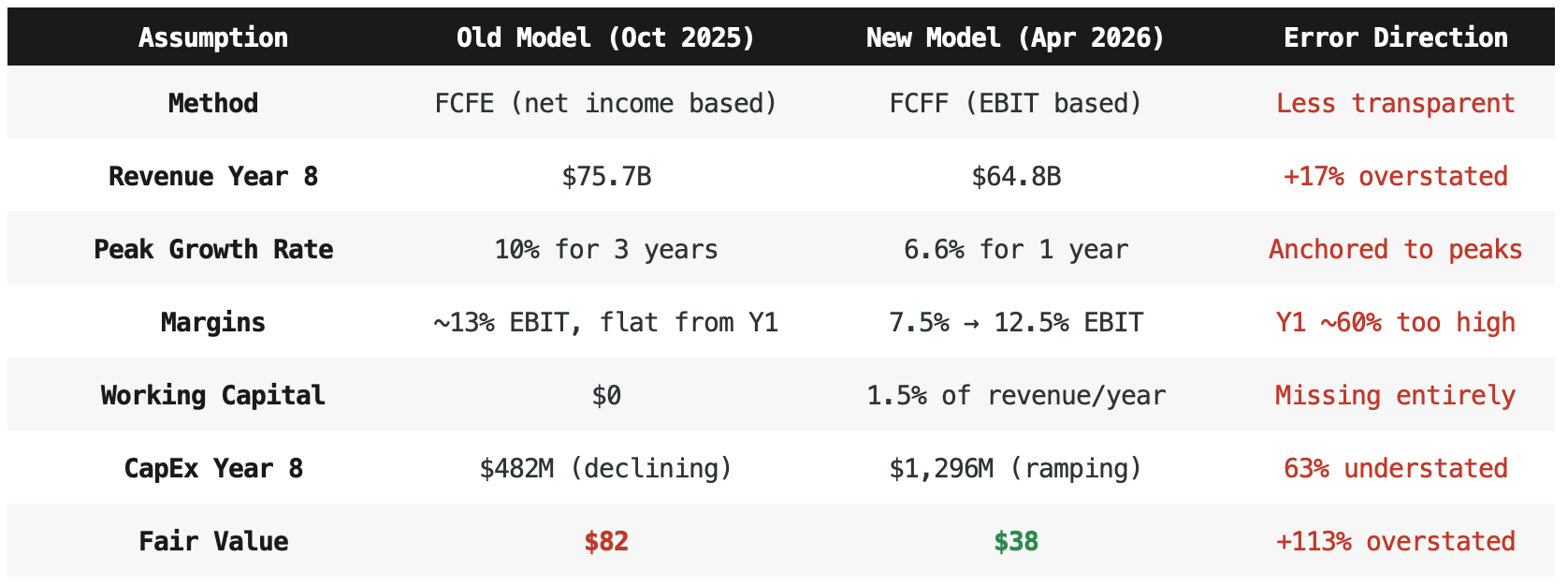

I used a simple FCF growth model. Conservative start - 5.5% growth while the turnaround plays out, then ramping to 10% as the recovery kicks in, then tapering back down to a 2.5% terminal rate. 9% WACC. Fair value: $77. At $55-56, that’s a 30% margin of safety. Textbook value entry.

I built a detailed Excel DCF.

Except it was wrong. By a lot.

What the new model says

Six months later, I rebuilt everything using an FCFF framework with segment-level revenue, explicit margin modeling, and actual working capital assumptions. Here’s the comparison.

Same company. Same public data. I was enthusiastic. After a decade of passive index funds, I was finally doing the stock picking thing again. I wanted to start buying. That energy is good for getting started. Less good for catching your own mistakes. The difference between these two models is not information - it’s questions I asked myself and answers I found.

The five mistakes

1. Real life is messy. Still try to model it.

On the revenue side, I actually did model a downturn - slow start, then ramp. I’ll show it below.

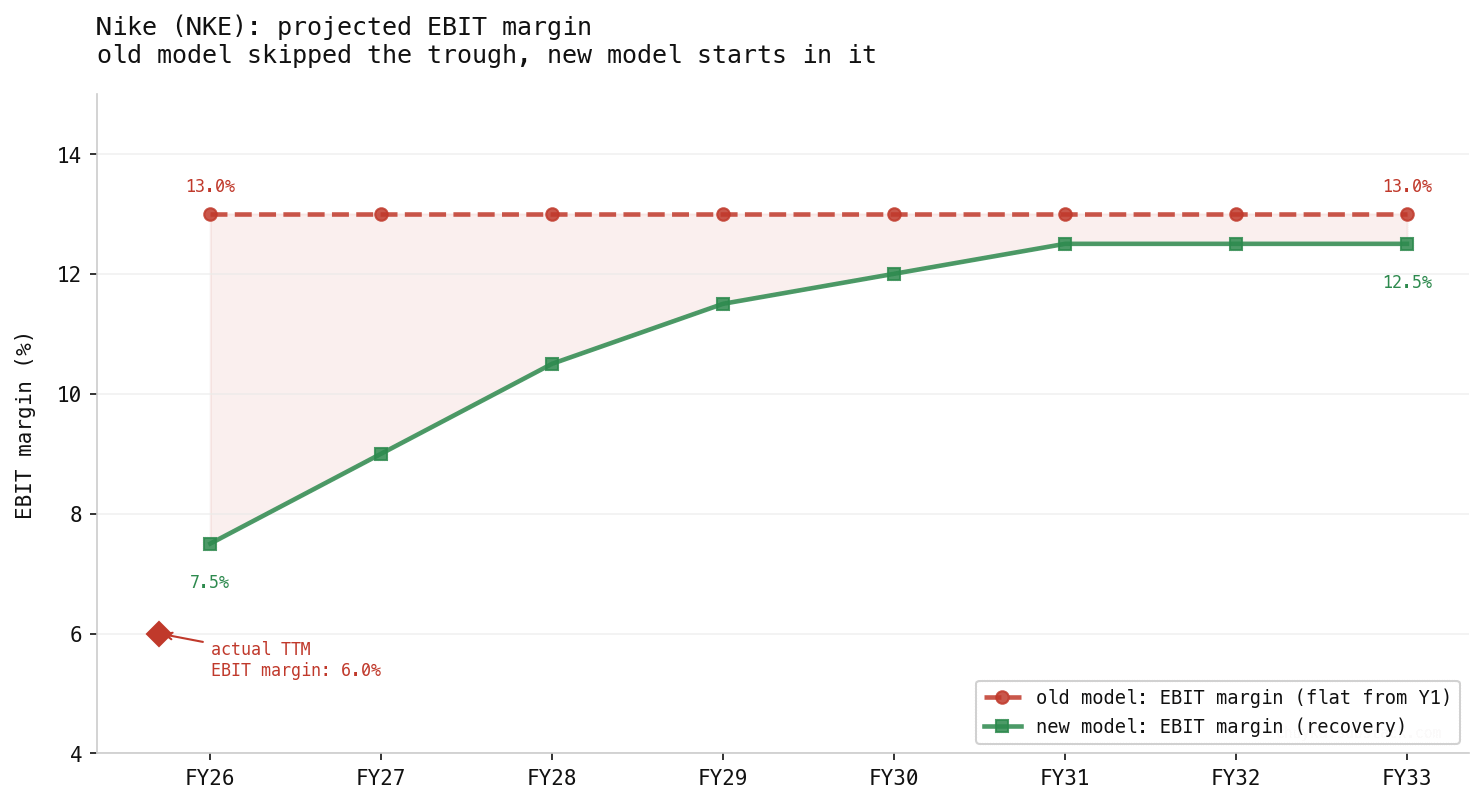

But on margins, I didn’t. I applied a flat 10% net margin from Year 1 through Year 8. No recovery curve. Just the destination.

Nike’s actual net margin was around 7% at the time. It has since fallen to 4.8%. The company was mid-CEO transition, reversing its DTC strategy, destroying $4 billion worth of classic franchise inventory, and eating tariff costs. All happening simultaneously. Every one of these drags on margins, and every one of them takes time to work through.

Look at the gap in the early years. That’s where the damage happens. The old model assumed 13% from day one while reality was sitting much lower and falling. The new model starts EBIT at 7.5% and takes six years to reach 12.5%.

The fix is to actually model the real world. Start at the current depressed level and build the margin back with specific drivers - NA wholesale returning, running category growing, classics cleanup finishing. Not the 13-14% Nike used to earn - tariffs make that ceiling unreachable now. 12.5% is the new normal in my opinion.

How did I calibrate the recovery speed? I looked at other consumer companies going through similar transitions. Lululemon’s 2013 CEO change cost 740 basis points of operating margin over three years. Gap lost 710 bps in its transition year. Under Armour lost 970 bps starting in 2022 and still hasn’t recovered. Even Starbucks, with arguably the smoothest handoff, lost 200 bps. These are all consumer brands with strong positioning. The pattern is consistent - 1 to 2 years of margin drag from decision paralysis, talent churn, strategy resets. Nike is doing CEO transition, DTC reversal, inventory cleanup, and tariff absorption all at the same time. Modelling instant recovery was fantasy.

The impact: Year 1 cash flow was overstated by roughly 60-80%. That’s $4.7 billion modelled vs $2.8 billion actual. Years 1-3 get the heaviest discounting in a DCF, but overstating them by that much still compounds through the whole model.

The lesson: If a company is changing strategy, don’t just model the final state. Try to understand how fast things actually move in the real world. Look for precedents - other companies that went through the same kind of transition. Study how their fundamentals reacted and how long the recovery took. History doesn’t repeat itself, but it sure rhymes. Use that rhythm to calibrate your model.

2. A growing business ties up more cash in inventory and receivables

I set change in net working capital to $0 for all eight projection years. So translating it to normal-people-speak - I was assuming it wouldn’t grow.

Think about what working capital actually is in a physical business. It’s sneakers sitting in warehouses waiting to ship. It’s invoices sent to Foot Locker and Dick’s that haven’t been paid yet. It’s the float between Nike paying its Vietnamese factories and collecting from its retail partners. That’s real money tied up in the physical operation of selling shoes.

When revenue grows, all of that grows with it. More shoes sold means more inventory in the pipeline, more receivables outstanding, more cash locked up in the cycle. Nike’s 11-year average is about 1% of revenue per year in incremental working capital needs. On $46-65 billion in projected revenue, that’s $500 million to $1 billion per year that the business absorbs before it becomes free cash flow.

Over eight years, ignoring this drained roughly $6-7 billion of cumulative cash flow from the model. That’s $4-5 per share in present value that simply didn’t exist.

The lesson: If the business is physical - it makes things, stores things, ships things, invoices customers - then growth costs working capital. The faster it grows, the more cash gets locked up. Model it as a percentage of revenue growth and check it against history. A $0 change only makes sense for a business that collects cash before delivering the product.

3. Build revenue from segments, not a single growth rate

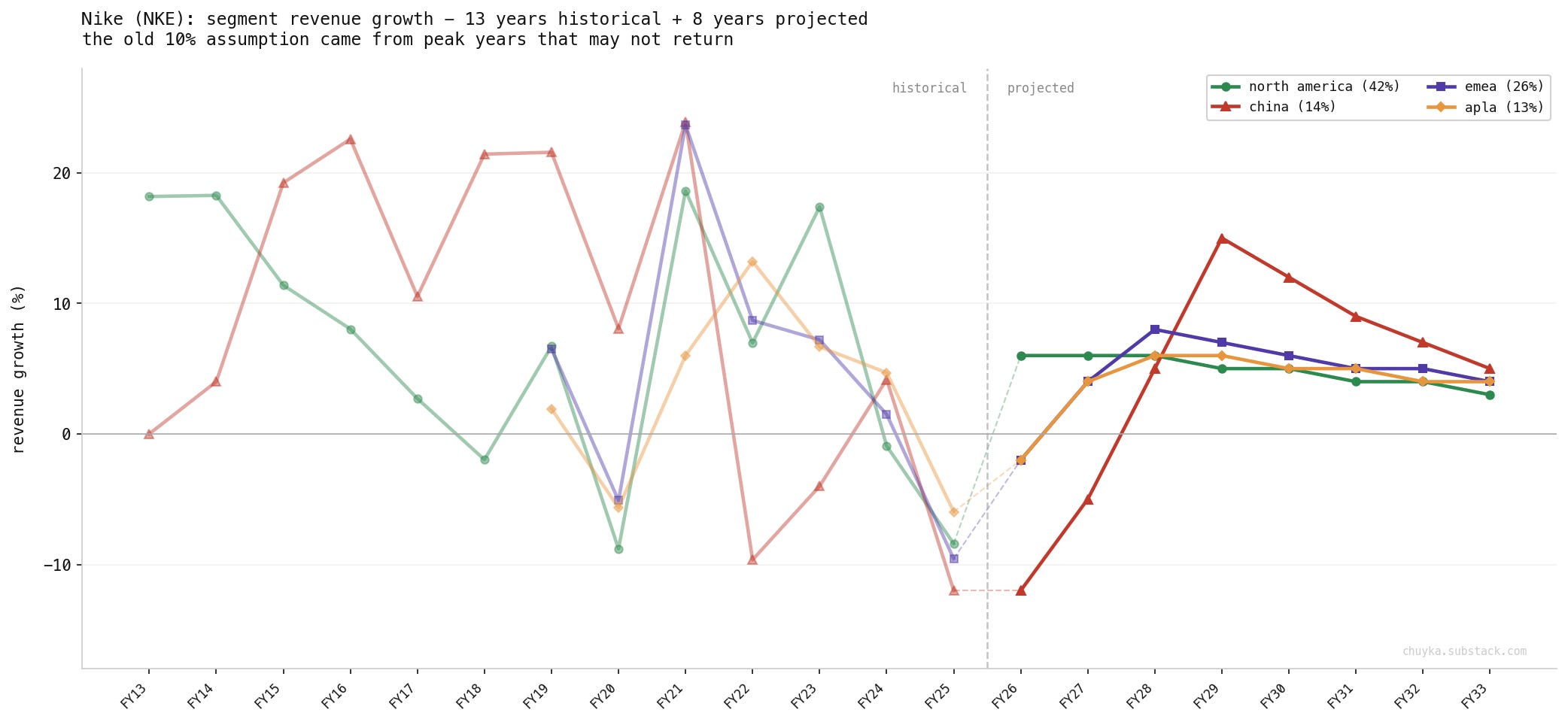

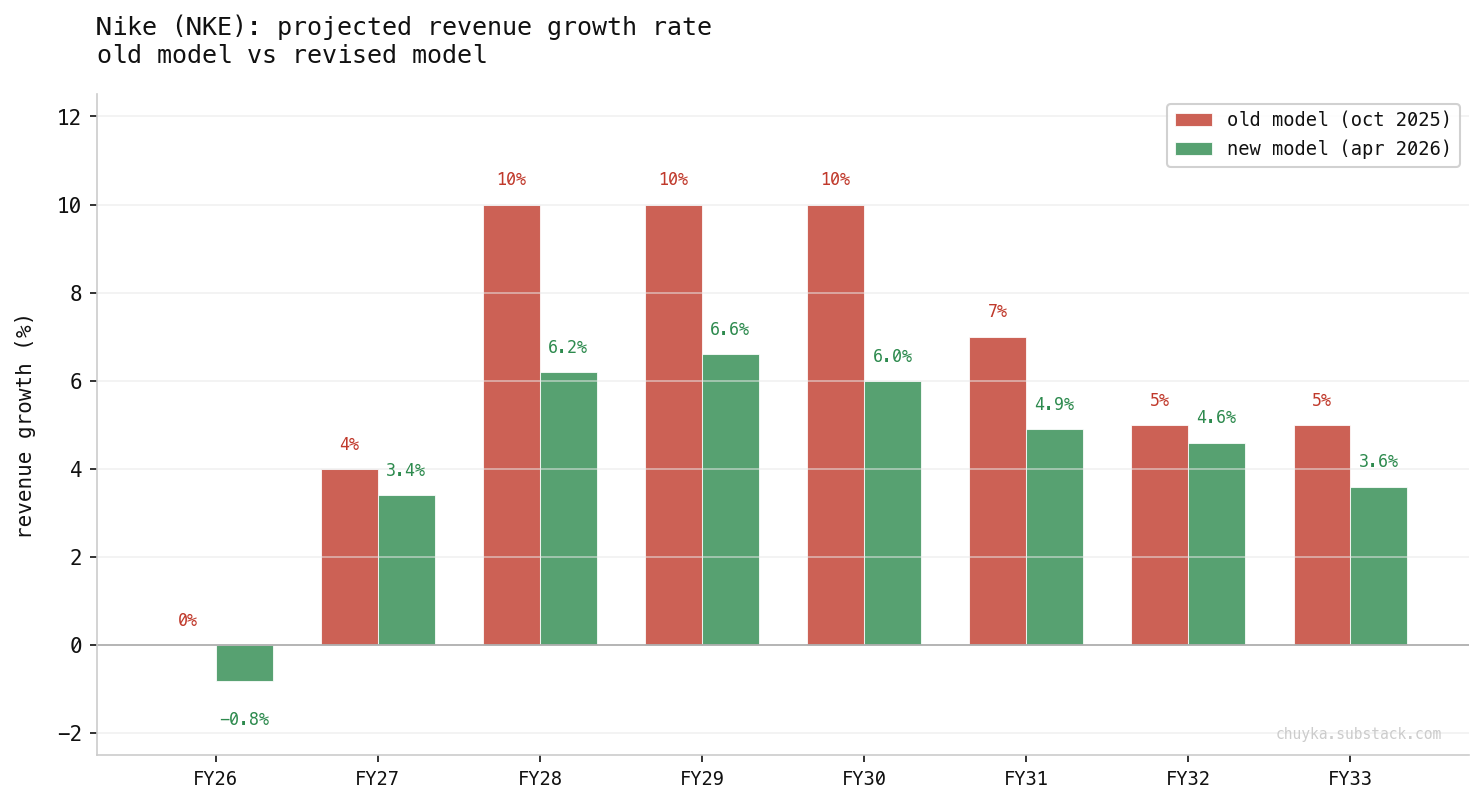

As I mentioned above - I did model the downturn. The old growth curve started at 0%, ramped to 4%, and only then hit 10%. I wasn’t ignoring the downturn on the revenue side. The problem was where I assumed the recovery would peak.

Where did 10% come from?

I looked at Nike’s history and anchored to the best years. FY2012 was +16%. FY2015 was +10%. FY2023 was +9.6%. The COVID rebound in FY2021 hit +19%. If you cherry-pick the peaks, 10% looks conservative. But Nike’s 15-year median growth is 6.0%. The 10-year CAGR ending FY2025 is 4.2%. I anchored to the highlights, not the average.

And there’s a deeper issue.

The Nike that grew 10% in FY2015 may not exist anymore. Hoka, On Running, and New Balance own the cultural moment in running and lifestyle. Nike’s sportswear market share fell from 15.2% to 14.1%. China - which was 18% of revenue at peak - is structurally losing ground to Anta and Li Ning with government propping them up. Converse is in decline with no recovery timeline. The competitive landscape shifted, and a single growth number can’t tell you that.

If you try to build revenue from segments to get 10% consolidated growth - it requires miracles from Nike everywhere at once. North America is 42% of revenue and realistically does 6% in a good year. China can spike to 15% in a recovery quarter, but it’s only 13% of the total. EMEA peaks at 8%. And Converse is declining.

Blend it all together and the consolidated peak is 6.6%. Not 10%.

Look at this chart. Thirteen years of history on the left, projections on the right. You can see exactly where the 10% anchor came from - North America hit 18% in FY2014 and FY2023. China was the growth engine at 20-24% in the mid-2010s. Those peaks made 10% consolidated growth feel conservative. But those peaks came from a different Nike in a different competitive landscape. The projections on the right are deliberately calmer. Five regions, five completely different trajectories. China goes from -12% to +15% and back. North America is the steady engine but it’s slowing. No single number captures this.

The difference in terminal revenue: $75.7 billion in the old model vs $64.8 billion now. Every dollar of that excess flows through to margins and cash flow.

There’s another benefit in building by segments I didn’t expect. And this approach applies to modelling as a whole.

When you model by segment (or disaggregate other compound numbers), you’re building around the same metrics management tracks and optimizes. Earnings calls show you where their eyeballs are. Hill talks about NA wholesale recovery, China store resets, running category growth - these are specific, measurable goals. If I model NA at +6% because management is focused on wholesale rebuild, I can check that against actuals every quarter. Did they hit it? Are they ahead or behind? The model becomes a scorecard for management execution, not just a fair value calculator.

A single growth rate gives you nothing to check against. “Did Nike grow 10%?” is a useless question. “Did North America wholesale recover while China stabilized?” - that’s a proper question.

The lesson: Build revenue and other compound numbers from components. A single growth rate invites anchoring to historical peaks. Bottom-up forces you to justify where each dollar of growth comes from. It’s much harder to be accidentally optimistic when every geography has to work on its own. And it gives you a framework to judge management against their own promises.

4. CapEx must be consistent with revenue growth

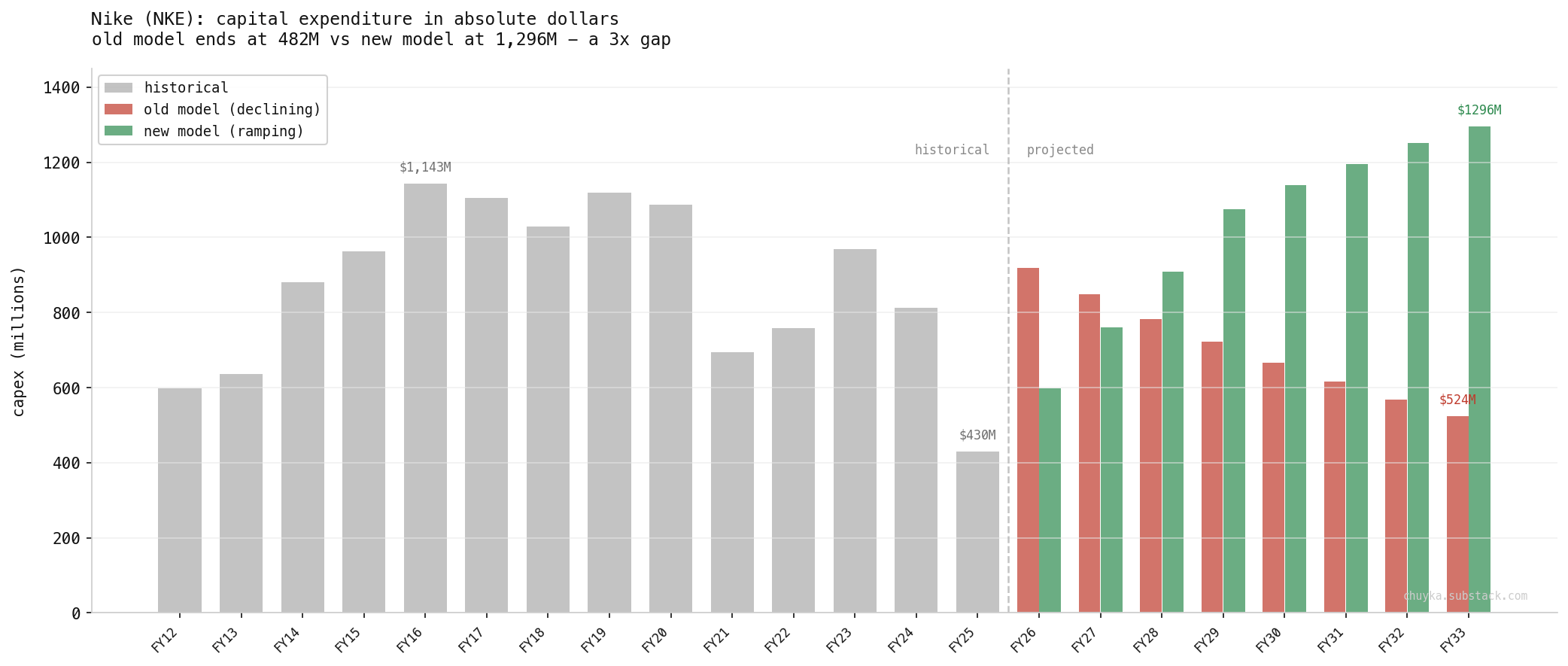

I started CapEx at $919 million and declined it to $482 million by Year 8. Nike had been cutting CapEx for years - from $1.1 billion to $430 million. I just extrapolated the trend (wtf.. why?).

But those cuts are just turnaround measures. Cash conservation during restructuring. $430 million was Nike’s lowest CapEx since 2003, when the company was one-third its current size. You can’t grow revenue from $46 billion to $76 billion while spending $482 million on property, equipment, and technology. That’s 0.6% of revenue. Below maintenance for a company with $7.5 billion in PP&E.

And think about where the money needs to go. Hill’s strategy is “elevated retail presentation” - making stores feel premium again after years of underinvestment. China has 5,000+ monobrand doors that management admits “aren’t compelling”. They’re running pilot store resets in Beijing and Shanghai that show better traffic and comp growth. That’s the playbook - but rolling it out across thousands of stores costs real money. Nike Digital needs investment too. You don’t rebuild a brand experience on a declining CapEx budget.

The history tells you everything. Nike spent $900 million to $1.1 billion a year on CapEx in its prime (FY2014-2020). Post-COVID it collapsed to conservation mode - $430 million in FY2025, the lowest since 2003. The old model extrapolated that decline to $482 million by Year 8 - below FY2012 levels when Nike was half its current size. The new model ramps back to $1.3 billion, which is just getting back to where Nike was in FY2016-2019. A 3x gap by Year 8.

The lesson: Don’t extrapolate CapEx cuts during a restructuring. If your revenue is growing and your CapEx is shrinking, your model is broken. Something has to give.

5. Know what your valuation framework hides from you

The old model used FCFE - Free Cash Flow to Equity. Start with net income, add depreciation, subtract CapEx and NWC, adjust for net borrowing. Discount at cost of equity. FCFE is a perfectly valid method. For certain companies - especially financials or stable businesses with predictable capital structures - it can be the right choice.

But every framework makes trade-offs in what it shows you and what it buries. FCFE starts from net income, which blends operating performance with tax strategy, interest costs, and one-time items. When net borrowing is in the cash flow, you think less carefully about reinvestment needs. The margin assumption? Buried inside a single net income number. Working capital? Easy to forget when it’s just one more line in an already blended formula.

FCFF - Free Cash Flow to the Firm - decomposes the business differently. EBIT margin is a line item. Tax rate is a line item. D&A, CapEx, and NWC each stare at you from their own row. For a turnaround story like Nike, where the whole point is tracking margin recovery and reinvestment needs, that visibility matters.

The FCFE framework didn’t cause the other four mistakes. But it made them easier to make and harder to spot. I think didn’t deliberately skip working capital - the framework just didn’t force me to think about it.

The lesson: Understand the weaknesses of whichever framework you use. Every method hides something. If you know what’s hidden, you can check for it. If you don’t, you’ll find out when the model breaks.

The one thing I got right

In the original post, I wrote about competition. Satisfy, Bandit Running, Tracksmith. Hoka. On. I personally switched from Nike running shoes to Hoka after an injury. And I liked them more than Nike. I said so publicly.

That qualitative insight was correct. Nike’s competitive position is weaker than it was five years ago, and the running category specifically has seen real share losses. My new model reflects this - North America growth caps at 6%, not 10%, partly because brands like On and Hoka aren’t giving market share back.

But here’s the thing. In October, I wrote about the competition in one section, then ignored it in the model. The spreadsheet projected revenue growth as if Nike was still the only game in town. The gut said one thing, the model said another, and I went with the model.

If your analysis identifies a real competitive threat and your model doesn’t reflect it, one of them is lying.

The dangerous model

The most uncomfortable part of this story isn’t that the model was wrong. It’s that it felt conservative.

Revenue growth was muted in years one and two. The discount rate was above 9%. Terminal growth was a cautious 2.5%. It looked careful. It looked skeptical. If you squinted at it, it looked like the work of someone who’d done their homework.

But “conservative on the things you can see” doesn’t help if you’re wrong on the things you don’t model. Zero change in working capital, instant margin recovery, declining CapEx, no segment decomposition - these aren’t aggressive assumptions. They’re missing assumptions. The model didn’t decide to be optimistic about working capital. It just forgot to include it.

The difference between a $82 fair value and a $38 fair value is not a difference of opinion. It’s a difference of rigor.

I’ve since rebuilt every model in my portfolio using the FCFF framework. Every position gets segment revenue, explicit margin paths, modeled NWC, and CapEx tied to growth. Two of the five came back looking different. Nike was the worst - you’ve seen the numbers. Lululemon (LULU) went from $283 fair value to $192 - a 32% haircut - once I modeled the CEO transition margin sag, tariff-adjusted working capital, and regional revenue build-up instead of a single growth rate. Same pattern. Same category of mistakes.

The process upgrade was worth more than any single stock pick.

So what now

This is the part I’ve been putting off.

I own 173 shares of Nike at $56.13. The stock is at $44. My updated model says it’s worth $38. I didn’t just buy at a premium to the market - I bought at a premium to my own revised fair value. That’s a $9,700 position in a stock I now think is overvalued.

The textbook answer is simple. Sell. The model says the stock is 14% above fair value. Take the $2,000 loss, redeploy the capital into something with actual upside, and move on. Sunk cost fallacy is the enemy. Be rational.

But it’s not that clean.

Nike is still Nike. The brand isn’t broken - the execution was. North America is growing again. Wholesale is +11%. Running is up 20% for three straight quarters. The product pipeline is the strongest in years. Hill knows the business - 32 years in, he’s not guessing. The turnaround is real, it’s just slower and more expensive than the market hoped.

My model gives Nike a 12.5% EBIT ceiling because of tariffs. But tariffs are political, not structural. If they ease - and my original thesis was that they would - the margin ceiling lifts and the fair value moves up. At 13.5% terminal EBIT instead of 12.5%, fair value jumps to mid-$40s. At 14%, it’s north of $50. The model is sensitive to this assumption because it affects every year of the projection.

So the real question isn’t “is Nike overvalued today.” It’s “what’s the probability that one or more of my conservative assumptions turns out to be too conservative.”

Here’s what I’m doing. I’m holding. But with conditions.

The turnaround has specific milestones I can track. NA revenue must stay positive. Gross margins must stay above 38%. EBIT margin inflection should show up by Q2 FY2027 - that’s management’s own timeline. China needs to at least stabilize. If these hold, I keep the position and let the thesis play out. If any of them break - especially NA turning negative again or margins deteriorating further - I sell. No averaging down. No adding. This is a position I need to earn my way out of through patience and monitoring, not through throwing more capital at it.

The honest version: I’m not confident enough to add, and I’m not panicked enough to sell. The model says one thing, the qualitative picture says something slightly different, and I’m going to let the next two quarters of earnings settle the argument.

Q1 FY2027 reports in late June. That’s the next checkpoint.

Chuyka check

Here’s what the numbers don’t capture.

I liked Nike. I wear Nike. I quoted Peter Lynch in the original post - “liking a store or a product is a good reason to get interested in a company.” And it is. But somewhere between getting interested and hitting buy, the analysis has to take over from the affection.

I did the work. I built a model. I found a margin of safety. But the work had holes in it, and the margin of safety was an illusion built on missing assumptions. The price looked right because the model was shaped to make it look right - not intentionally, but through omission.

My chuyka on this one was wrong. Not because the gut read was bad - Nike is still a great brand with real competitive advantages. But because I let the gut substitute for math in places where the math mattered.

The next time I feel strongly about a company, I’ll still listen to the feeling. That’s the whole point - data gets you 90% there, chuyka gets you the rest. But I’ll also double-check that the model doesn’t have any convenient blind spots where the feeling is doing the work the spreadsheet should be doing.

Trust your chuyka. Don’t let FOMO eat you alive.

Not investment advice. Think for yourself. Don’t trust online experts.